Kremlin looks to squeeze oil companies for cash

Hello! This is Alexandra Prokopenko with your weekly guide to the Russian economy — brought to you by The Bell. In today’s newsletter, we’ll look in depth at how Russia wants to get more tax from oil exporters — and why these companies might be making more money than many think. We also look at why bilateral attempts to encourage India-Russia wartime trade in rupees are falling flat.

Russia’s ‘new formula’ to increase tax revenue from oil exporters

The Russian authorities continue their efforts to balance the books: after demanding funds from big businesses, they are now looking at oil companies. In particular, the Finance Ministry is changing the way it calculates taxes for oil companies. Instead of relying on prices from energy agency Argus, which currently shows a $40 discount on Russia’s Urals blend compared to benchmark Brent, the ministry will use its own formula.

The new formula

The Finance Ministry has introduced legislation that will change the rules for calculating taxes on oil companies. At present, the ministry bases Mineral Extraction Tax (MET) and other oil taxes on the market price for Urals crude in the European ports of Rotterdam and Augusta, as reported by Argus. These are the same prices that the ministry publishes every two weeks as its “average price for Urals oil.” The discount on Urals compared to Brent is derived from these figures. Since the European oil embargo came into force late last year, the price for Urals has dropped, and the discount to Brent increased to up to $40 per barrel.

From April 1, the Finance Ministry will abandon Argus’ prices altogether. The Urals prices will still be pegged to Brent (this, by the way, explains which the much-discussed alternative Russian benchmark is not a viable option). But the discount will now be set by the Russian authorities. Initially, the discount will drop to $34 per barrel and it will continue to fall step by step until it reaches no more than $25 per barrel in July. This will increase the tax burden on oil companies and help ease Russia’s budget deficit. That deficit is increasing in part due to a fall in oil and gas revenues — last month they were down 46% year on year.

Under the new arrangements, Russia is expected to gain up to 700 billion rubles ($9.4 billion) in additional revenue. Moreover, the government will cut subsidies on gasoline and diesel fuel, raising between 150 billion rubles and 300 billion rubles in additional funds. The overall revenue gain is expected to be as much as 1 trillion rubles ($15 billion).

The Finance Ministry’s proposed legislation is a compromise agreed between the government and the oil industry. Initially, the proposals were much tougher: the ministry wanted to cut the discount to $20 and impose the changes as quickly as possible. That rush was prompted by the record budget deficit in January that forced the authorities to sell yuan from the National Welfare Fund and borrow on the markets.

Combined with an announced reduction in oil production, the new formula will help the Finance Ministry raise the 8 trillion rubles ($115 billion) in oil-and-gas revenues envisioned in the 2023 budget. Economist Alexander Isakov of Bloomberg Economics Russia calculated that, if expenditure and non-oil and gas revenues come in as planned after the implementation of the new formula, the overall budget deficit will be just 4.3 trillion rubles. That’s not far off the government’s planned 2.9 trillion ruble deficit.

Can the oil companies pay?

With Western sanctions and an enforced pivot towards Asian markets, Russian oil companies may not seem like an obvious cash cow. However, some believe they are not suffering nearly as much as advertised. Since the European Union imposed its oil embargo, the Russian oil market has been extremely opaque — and analysts suspect that companies are, in fact, selling at a discount far less than the publicized $35-40.

Sergei Vakulenko, a non-resident fellow at the Carnegie Endowment for Peace, has explored this theory in at least two articles, arguing that the Argus prices for Urals lost any meaning after the start of the war. Up until Dec. 5, when Russian oil was still exported to Europe, it was profitable for Russian oil companies to sell at a low price: they could offload cheap crude to their own refineries and then sell the resulting oil products at full market price in Europe. As a result, he suggested, oil companies avoided taxation, circumvented sanctions and made money trading with Europe.

Once the European embargo came into force, Vakulenko believes a similar story began to unfold in Asia. Based on analysis of public data and conversations with traders, he suggested that Indian buyers were getting Russian oil at a maximum discount of $10 per barrel, rather than the headline $30 to $40 figure. An analyst at a leading investment bank who spoke with The Bell and said he believed Vakulenko. Much of the difference has been pocketed by trading and shipping companies connected to Russian oil majors.

To some extent, Western sanctions have succeeded in making Russian exports less transparent not only for the West but also for the Russian government, Vakulenko told The Bell. “Circumstances have created an enormous rent-capturing opportunity at the expense of Russian state coffers and the European consumer”, said Vakulenko. “The Russian state was deprived of a substantial share of oil revenue.”

The new formula put forward by the Finance Ministry should reduce incentives for oil companies to manipulate prices and oblige them to pay more tax.

Why the world should care

High spending and a fall in revenue is one of the biggest financial challenges facing the Russian government this year. There will be no repeat of the oil-and-gas bonanza of spring 2022, which largely canceled out the early impact of sanctions. Russia’s technocrats officials will have to show ever greater ingenuity and persistence to fill the state’s coffers without stifling the economy. Of course, there is little they can do to change the primary cause of economic uncertainty and rising expenditure — the war in Ukraine.

Dear readers,

The Bell is now listed as “a foreign agent” in Russia: we can no longer raise money through advertising, and our business model is in ruins. Journalists in Russia face greater risks than ever before. Repressive new laws threaten up to 15 years in jail for objective reporting.

However, we are not about to give up. This newsletter is our newest project. It presents an in-depth analysis of the Russian economy, which has survived the first year of the war but is becoming ever more secretive. We will try and shed some light on what’s going on. Each edition will tackle a part of the big question: how long can the Russian economy endure under sanctions and when will the Kremlin run out of money for its war?

We don’t want to have to charge a fee for our newsletters. However, if The Bell is to continue its work, we need your support.

You can make a donation here. It will help our journalists continue investigating stories, breaking news and publishing newsletters.

Attempts to boost trade with India in rupees are not working

A mechanism of trading in rupees via so-called “vostro” accounts between Russia and India has turned out to be of little interest to traders or banks, Bloomberg reported this week. The first international transactions using vostro accounts (a type of account that a domestic bank holds for a foreign bank in the domestic bank’s currency — i.e. rupees) were reportedly used by India last year to import Russian military hardware.

India’s refineries, which have purchased record levels of Russian oil, prefer to pay in Arab dirhams, according to Reuters. And the vostro account mechanism is not appropriate for Russian banks because of an imbalance in foreign trade — they simply don’t want excess rupees piling up. According to Indian trade statistics cited by Bloomberg, imports of Russian goods were 16 times greater than Indian exports in the first eight months of the Ukraine war. According to Bloomberg, officials from both countries have discussed ways of encouraging Indian exports to Russia to redress the imbalance — but to little avail.

The lack of interest comes despite Russia and India introducing a special settlement mechanism designed to: the Indian regulator allows authorized banks to open vostro accounts in rupees in Russian banks. This allows Indian importers to make payments to these accounts in rupees — and these accounts can also be used to pay Indian exporters in their national currency. Any surplus that accumulates can, in theory, be invested in Indian government bonds or in state investment projects.

For Russia, creating a mechanism for international trade that does not rely on reserve currencies (especially the euro or the dollar) is increasingly urgent. Even those companies not directly affected by sanctions face enormous problems settling with foreign counterparts. Accounts in dollars or euros can be blocked, while foreign currency payments move slowly and even banks in “friendly countries” can block transactions. The Central Bank announced on Wednesday that it was setting up a new department to work on international settlements.

India has not joined the West in sanctions against Russia and is keen to buy Russian oil and related products at discounted rates. However, the country’s strict currency laws are not making it easy to boost bilateral trade. The rupee is not a fully convertible currency, importers require special permissions from India’s Central Bank, and many sectors of the economy are not open for investment to non-residents.

Why the world should care

Sanctions are forcing Russia to look for reliable ways of making large international payments. India is just one example. Creating an alternative infrastructure takes years, and time is not on Russia’s side. This situation also highlights the barriers raised by capital flow restrictions: without such restrictions, Indo-Russian trade would develop much faster.

Figures

As of Jan. 1, Russians held 6.63 trillion rubles ($94.3 billion) in deposits in foreign banks. This figure more than trebled in 2022 as Russians put $63.7 billion into foreign accounts, Central Bank statistics suggest. This is the biggest increase in deposits to foreign banks since the Central Bank began publishing these statistics in 2018.

Weekly inflation in Russia (Feb. 7-13) slowed to 0.18% against 0.26% for the previous week, according to State Statistic Service figures. Annual inflation slowed from 11.72% to 11.61%.

The population’s savings at the start of January reached a historic high of 88.9 trillion rubles and a monthly increase of 6.6 trillion rubles was also a record, according to the Solid Figures Telegram channel. Savings in rubles increased by 3.6 trillion, with a further 3 trillion put into foreign currencies. It appears that the heightened economic and political uncertainty is discouraging Russians from spending.

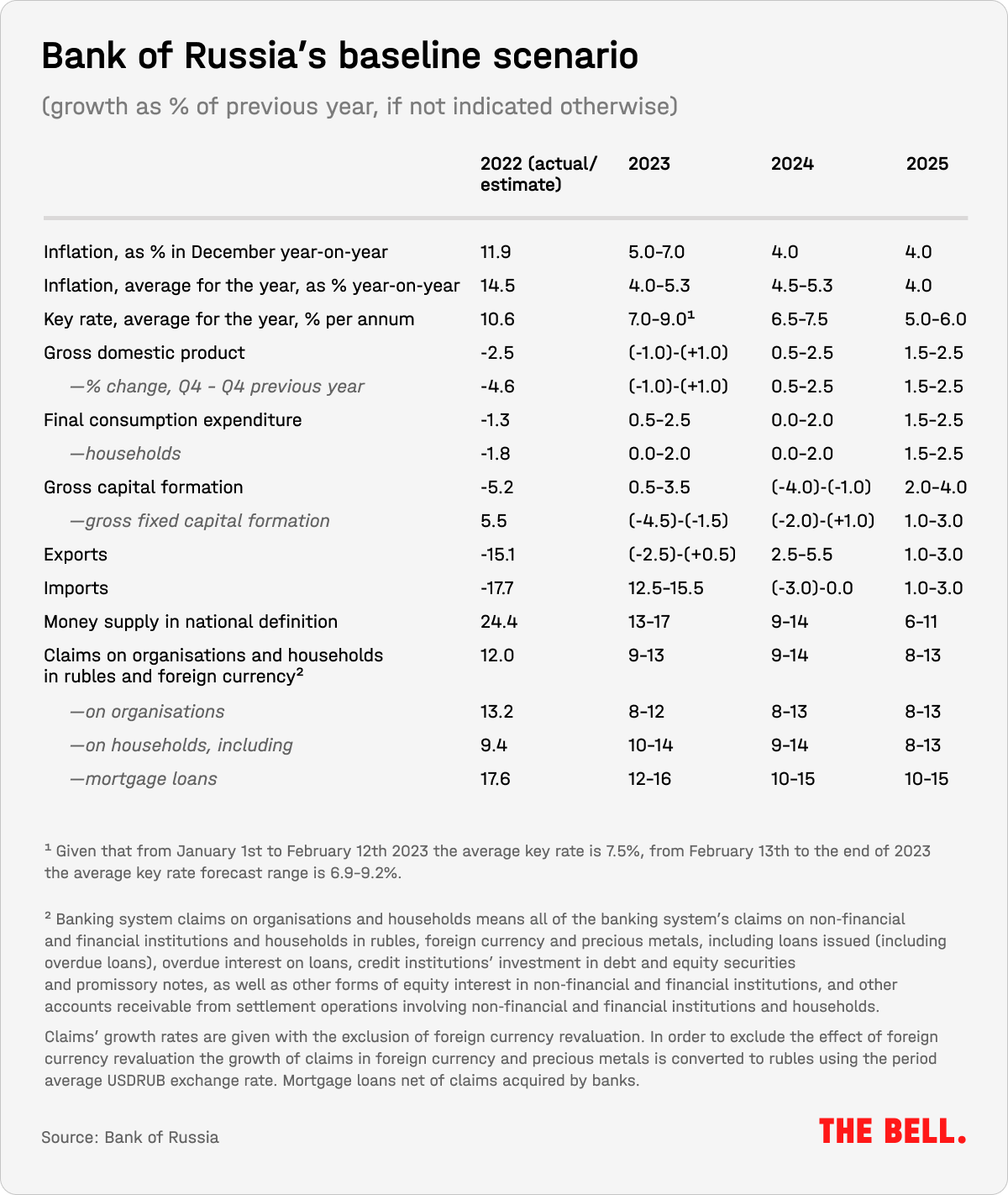

At the end of last week, the Central Bank increased its forecast for its base rate to 7-9%. That signals a willingness to tighten monetary policy in response to inflationary risks. The Central Bank also adjusted its mid-term forecasts:

What to watch for this week:

- Vladimir Putin will give his state-of-the-nation address on Feb. 21. You can read more about this major political event here.

- The Central Bank will release a report on monetary policy (Feb. 20)

- Data on industrial output for January (Feb. 22)

- Extraordinary meetings of the State Duma and Federation Council (Feb. 22)

- The first assessment of GDP in 2022 by Rosstat (Feb. 22)

Further reading:

- Could Russia and China emerge as world leaders? A report from the Munich Security Conference on the contradictions in the global order exposed by the Ukraine war;

- Man vs. Myth: Is Russia’s Prigozhin a Threat or Asset to Putin? Tatiana Stanovaya discusses the extent to which Evgeny Prigozhin helps or hinders Putin;

- Finland’s Central Bank summarizes the shape of Ukraine’s economy before and during the first ten months of the war — and gives some preliminary thoughts about the shape of the country’s post-war economy.

{kind=link}