Russia’s wartime budget

Hello! This is Alexandra Prokopenko with your weekly guide to the Russian economy — brought to you by The Bell. Today's top story is an analysis of Russia’s 2024-2026 budget, which foresees a record level of military spending. We also look at a proposal to make the Russian ruble more like the Chinese yuan by introducing a distinction between domestic and offshore trading.

Russia’s 2024-2026 budget includes record military spending

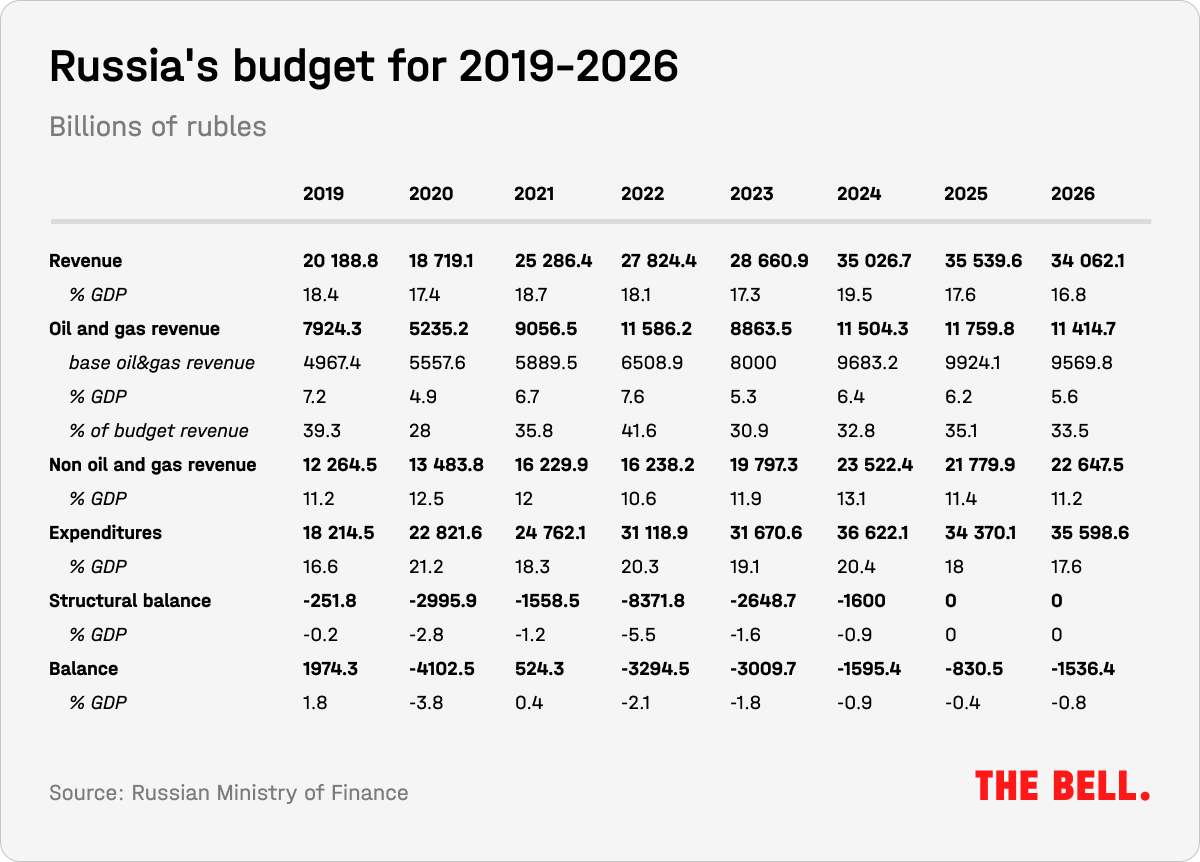

Russian Finance Minister Anton Siluanov chose to use Soviet-era language when talking about the country’s recent budget. “It has everything for the front, everything for victory,” he said, referencing a World War II slogan. It is a budget dominated by military expenditure. And it is a window onto the government’s priorities: financing the war in Ukraine, spending on the security services, integrating occupied Ukrainian territory and social handouts. For the first time in modern Russian history, more has been allocated to military expenditure than social spending.

Where’s the money coming from?

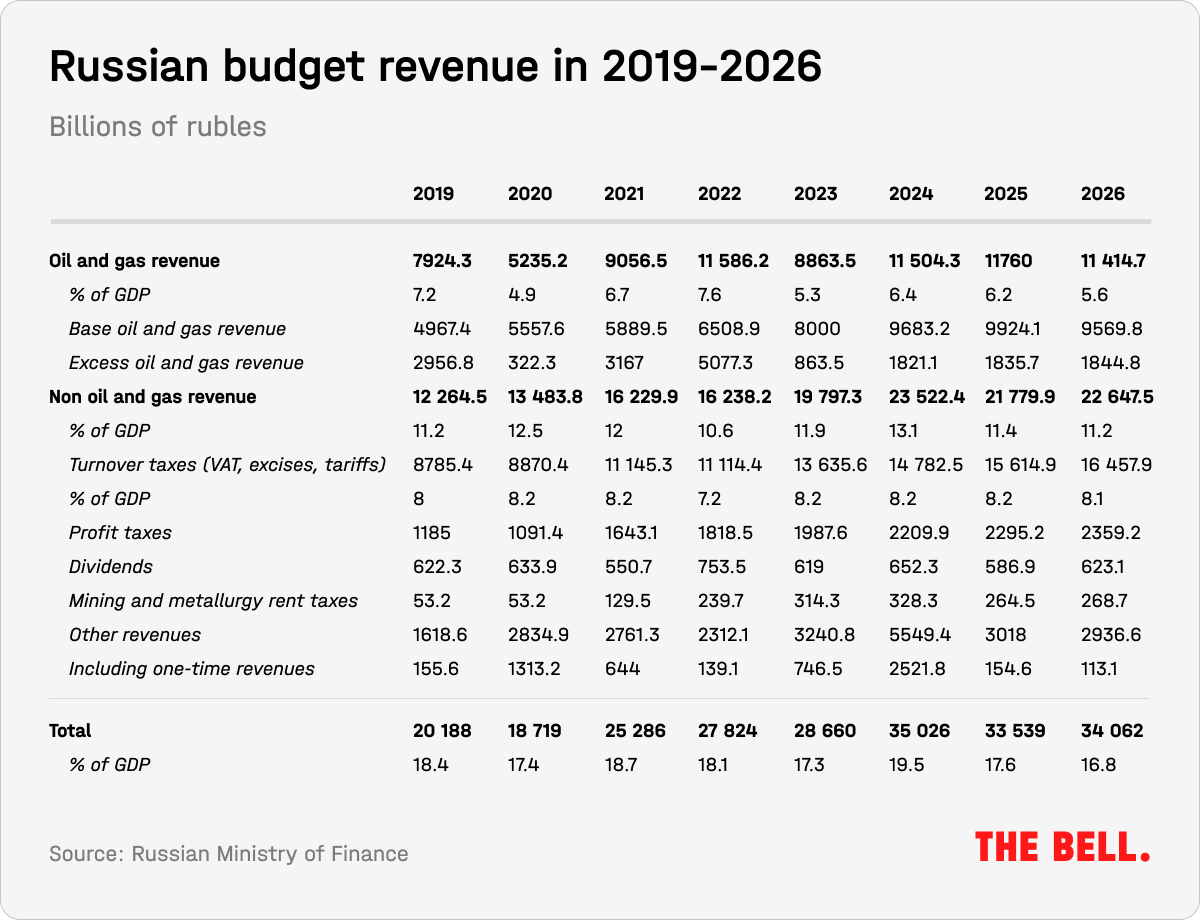

The Russian government this week finalized the budget for 2024-2026 and submitted it to the State Duma for approval. Particularly striking are the plans for revenue collection: in 2024 the government is expecting to raise 35 trillion rubles (34% more than this year). This is based on the Economic Development Ministry’s optimistic forecasts for 2024 when they predict 2.3% GDP growth, oil prices to average $85 a barrel and the average U.S. dollar exchange rate to be 90.1 rubles. Interestingly, the Central Bank’s forecasts are far more conservative (it anticipates up to 1.5% GDP growth and oil at $60 a barrel).

Raising so much money seems an incredible goal while President Vladimir Putin continues his war in Ukraine and Western countries and their allies prepare more sanctions. But the Kremlin is assuming that, at the very least, Russian oil will continue to be sold to India and China; the Western price cap on Russian oil will not change (and will continue to be ineffective); Western countries will not risk further oil embargoes; and that the oil price will remain high. Nor does the government expect any new restrictions on imports.

Non oil-and-gas revenues next year are projected to make up 13.1% of GDP in 2024. Here, the government is largely relying on continued economic growth, and thus a rise in domestic demand, which will push up VAT revenues. There will also be sizable one-off inflows, including a windfall tax on big business.

Private business is also providing a chunk of this money. Russian private business can feel justifiably badly treated as — in the wake of Western sanction and the economic turmoil at the start of the war — its adaptability helped the Russian economy survive and re-orient to new markets. Now, it’s seen its tax burden increase significantly.

Historically, economic rents in Russia have been unfairly distributed and the Finance Ministry argued this week that new export duties — one of the sources of revenue for the budget — “will contribute to some improvement in the fairness of the distribution of rental income in these industries.” These new duties have not been widely discussed with companies and, along with the windfall tax, effectively amount to a tax rate for some in excess of 50%.

How will it be spent?

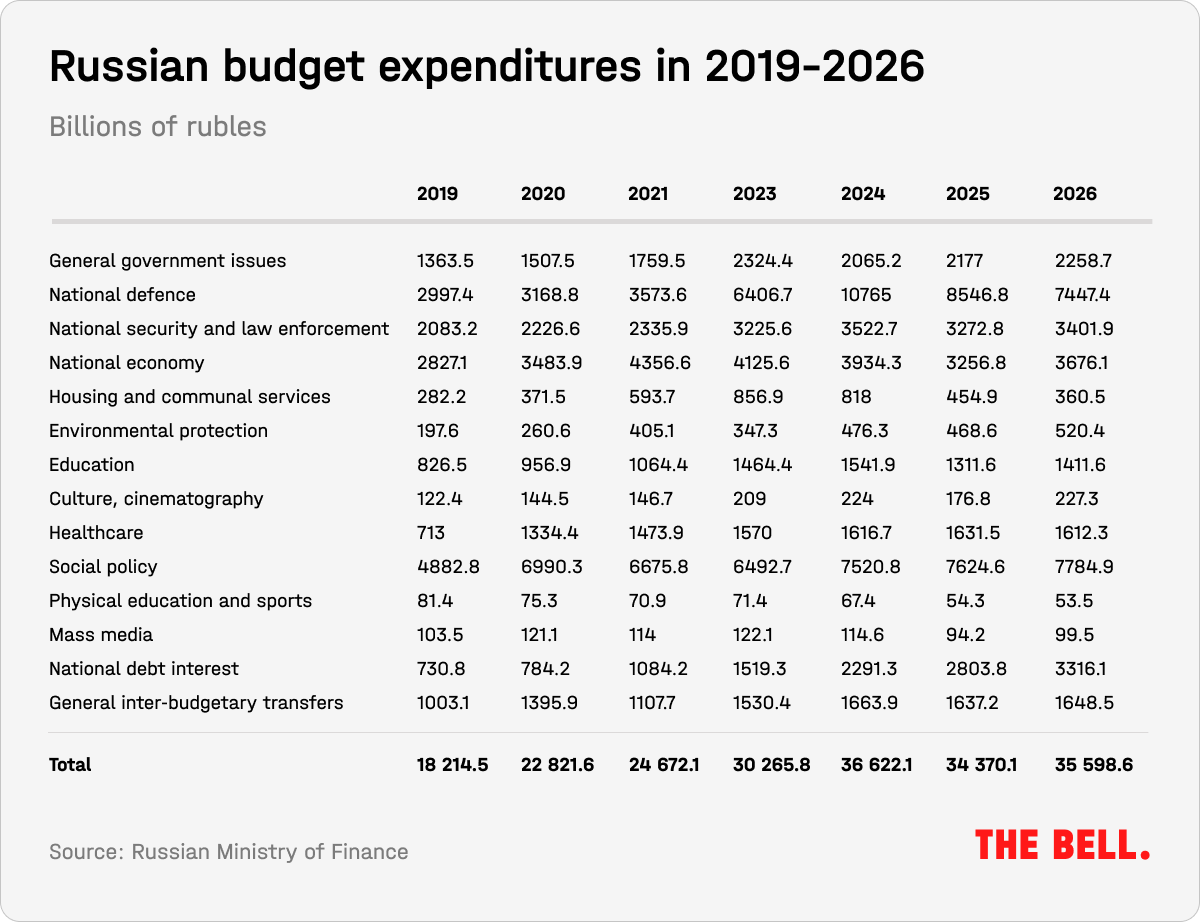

Spending in 2024 is estimated at 36.6 trillion rubles (up 26.2% on the year before). This means that the budget deficit will be significantly reduced — from 2.9 trillion rubles planned this year to 1.6 trillion rubles in 2024.

The increased military spending is not just about producing more hardware, Pavel Luzin, a military expert at the Fletcher School told The Bell. By earmarking almost 11 trillion rubles for the military, the government is trying to price in the added costs of endless import substitution, the operational inefficiency of the defense sector, and large payments to soldiers and the families of those killed in action in Ukraine.

Spending on the war and the occupied territories of Ukraine also appears in other parts of the budget. The increase in social spending is partly linked to the war. For example, Putin recently ordered the creation of the “Defenders of the Fatherland” fund that will assist combatants (contract soldiers, conscripts, mercenaries) with medical treatment and reintegrating back into society. The fund will be largely paid for with federal money.

The government will also invest large amounts in the Ukrainian territories captured by Russia since the full-scale invasion. The budget even has a separate section for the socio-economic development of these regions: to rebuild what Russia itself destroyed, 37.5 billion rubles will be allocated in 2024. However, far more will be channeled to the occupied territories via interbudgetary transfers. In 2023, they have already received a total of 483 billion rubles from the federal budget as non-reciprocal transfers. In 2024, subsidies to the regional budgets will increase by 178 billion rubles, and most of the money will go to the occupied regions, Vedomosti reported.

The inflation riddle

One of the most baffling parts of the budget is the low projected inflation rate for 2024. The government apparently expects just 4.5% inflation despite also planning a 34% increase in expenditure, a weakening ruble, and an increase in tariffs. The government also expects there to be an increase in real disposable income (2.7%) and salaries (2.5%) amid a labor shortage; a dynamic that would normally be expected to push inflation up.

With so many inflationary factors, the only way inflation could be kept to somewhere near 4.5% is if the Central Bank keeps interest rates high (they are currently 13%). The regulator has already warned parliament that this is what is likely to happen in the medium term.

What comes next?

The Finance Ministry believes that, in 2025, there will be no need to spend so much on the military and the defense sector. From this point, the government will return to its familiar budget rules to limit expenditure. However, this seems more like wishful thinking than realistic analysis. Neither the Finance Ministry, nor the government, knows how and when the war will end, or whether the West will impose more effective sanctions on Russia to reduce its revenues. In addition, oil prices are fundamentally unpredictable.

Why the world should care

By relying on military spending, the Kremlin will continue to push the economy into the trap of “eternal war.” As time goes on, it will be increasingly difficult to keep financing the war without hitting standards of living. And other surprises cannot be ruled out: for example, tax hikes or a new round of mobilization. The presidential election early next year, which Putin is set to win, will open a window of opportunity for the Kremlin to make unpopular decisions.

A two-tier Chinese model for the Russian ruble?

Economic Development Minister Maksim Reshetnikov this week reignited discussions about controls over the cross-border movement of capital. Apparently the Economic Development Ministry is planning to combat ruble volatility with the “Chinese method,” creating what Reshetnikov describes as a “membrane” between domestic and international ruble markets.

China’s two-tier model of currency regulation emerged at the start of the country’s market reforms. It was designed to protect the domestic market from speculation and exchange rate turbulence caused by sudden inflows and outflows of capital. It also makes it more difficult for companies – domestic and international – to withdraw money earned in China.

In effect, it means that the yuan is divided in two. The domestic yuan (CNY) is legal tender in the People’s Republic and the exchange rate is set by the National Bank of China. Then there is the offshore yuan (CNH), which is held in foreign bank accounts and can be traded on currency exchanges. This makes it possible to separate flows linked to day-to-day business (current accounts) and investment of speculation funds (capital accounts).

It is the increasing supply of rubles that led Reshetnikov to look to China. According to the minister, 41% of current export earnings are in rubles, part of which is then converted back into foreign currency, or goes into foreign accounts. “This means we have a foreign exchange market abroad,” Reshetnikov explained.

If the minister has a detailed plan to implement the Chinese model in Russia, he isn’t sharing it yet. But its implementation would mean moving away from a fully convertible ruble. The Central Bank traditionally opposes any steps in this direction. And Putin has always regarded a fully convertible ruble as one of his main achievements.

Nobody knows how ditching a convertible ruble would impact the economy. We can say with some confidence it would undermine already shaky faith in the national currency and complicate import-export operations. The impact on foreign investment would not be large, since this has almost disappeared since the invasion. However, it’s also likely that it would create an entire market for semi-legal currency transactions. Sooner or later, this market would inevitably come under the control of one of Russia’s security services.

Perhaps most importantly, the government's attempts to regulate the capital flows and the exchange rate could undermine confidence in the independence of the Central Bank — and likely cause problems for the ruble.

Inevitably, Reshetnikov was not willing to discuss the underlying reasons for the increased demand for currency — which are the war, Western sanctions and the explosion of public spending.

Why the world should care

It’s possible that these sorts of discussions about the ruble may eventually turn to the possibility of further capital restrictions. If this is seen as a real possibility, it could lead to businesses and individuals rushing to transfer capital anywhere they can, as soon as possible. If panic sets in, that could spark precisely what Reshetnikov is seeking to prevent — increased capital outflow and further depreciation of the ruble.

Key figures

Inflation in Russia was 0.28% from Sept. 19 to Sept. 25. Since the start of the year, consumer prices in Russia have risen 4.32%, according to the State Statistics Service.

The value of mortgages issued in August was 860 billion rubles, an all-time record. It’s possible next month could be another record-breaking month with over 1 trillion rubles worth of mortgages. In 2012, the annual value of mortgages issued was 1 trillion rubles.

The Russian ruble is now the main currency for export payments. In 2023 its share of expert payment increased threefold to 40%, reported media outlet RBC. In total, 72% of export payments were made in rubles or the currencies of so-called “friendly countries” (at the start of 2022 it was not more than 15%).

Further reading

Azerbaijani Control of Nagorno-Karabakh Will Not Stop Conflict in the South Caucasus, argues Vladimir Solovyov

Loud complicity: Why Russian officials are breaking their silence on Ukraine, explains Mikhail Komin

The Ideology of Putinism: Is It Sustainable? asks Maria Snegovaya, Michael Kimmage, and Jade McGlynn

The author of this newsletter is one of Russia’s leading writers on this topic: independent economic analyst Alexandra Prokopenko. Alexandra worked as an advisor at Russia’s Central Bank and Moscow’s Higher School of Economics from 2017 to 2022 — and before that she was an economic journalist for Vedomosti, then Russia’s leading business newspaper. Today, Alexandra works as a researcher at Center for East and European Studies (ZOiS) in Berlin a non-resident scholar at the Carnegie Endowment for International Peace and a visiting fellow a the Center for Order and Governance in Eastern Europe, Russia, and Central Asia at the German Council on Foreign Relations. She holds an MA in Sociology from the University of Manchester.

{kind=link}