Sberbank vs. Yandex

Hello! This week our top story is about the big changes for Russia’s online services sector as internet giant Yandex and banking giant Sberbank go head-to-head. We also look at the beginnings of a coronavirus second wave, and the architecture of a radical new approach to economic policy that is taking shape in the government.

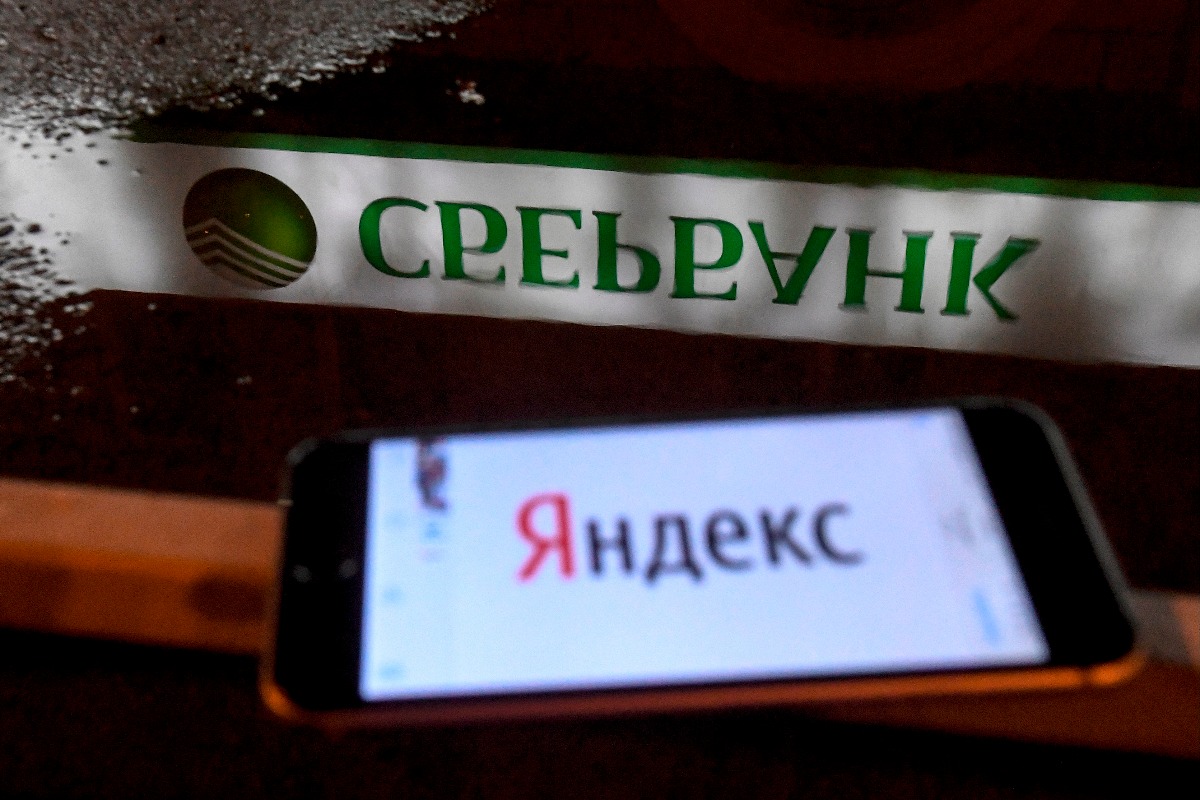

All change! Yandex becomes a bank, Sberbank turns to tech

It was a big week for the Russian tech market. Internet giant Yandex, dubbed the ‘Russian Google’, took a big leap into the financial sector with the announcement of plans to purchase digital bank Tinkoff for $5.5 billion. Days later, the country’s largest bank, state-owned Sberbank, launched a major rebranding in which CEO German Gref gave a Steve Jobs-esque presentation claiming the company was no longer a bank but a tech ecosystem.

- After Sberbank and Yandex’s failed attempt to build a ‘Russian Amazon’ and Sberbank’s unsuccessful bid to swallow Yandex, the two companies are archrivals. While Yandex started out as a search engine, Sberbank was a vast, unwieldy bank with a Soviet heritage and a reputation for nightmarish bureaucracy. But both have successfully reinvented as the two undisputed market leaders in online services. Mail.ru, Russia’s second largest internet company after Yandex, formed a joint venture with Sberbank in 2019 to provide food and taxi services, selling the bank a 21 percent voting share in the process; and Sberbank owns a controlling stake in the country’s third biggest internet company, Rambler Group. Yandex and Sberbank are facing up for a battle.

- Russian internet companies appear to be developing along Chinese lines, rather than following the U.S. model. In other words, they bring together the greatest possible number of different services under the banner of one super-provider, like Alibaba or Tencent. Yandex is a market leader in search engines, ride-hailing, carsharing and food delivery, while also having its own online marketplace, and audio- and video-streaming services. The only thing missing was an internet bank. While Yandex was Sberbank’s partner, the tech giant was barred from dabbling in financial services. But after their separation earlier this year, Yandex was free to make its move.

- Tinkoff Bank was an obvious takeover target. Set-up in 2006 by Russia’s best-known entrepreneur, Oleg Tinkov, it was the country’s first purely online bank. It seemed like a crazy idea at the time, but Tinkov turned out to be visionary. By 2020, it was a top 20 Russian bank, while its user-friendly share trading app enabled it to profit from the boom in private investment. The Tinkoff brand has been an icon for many young Russians.

- This year has been a highly profitable one for Tinkov’s businesses. His bank saw its profits increase 25 percent in lockdown, while his brokerage company gained a million new clients and saw a fivefold rise in the funds under its management. But Tinkov himself has had big problems. In February, it emerged that the U.S. tax authorities wanted to charge Tinkov, a former U.S. citizen, with hiding $1 billion of taxable revenue. Tinkov, who now lives in London, was arrested and bailed. A few days later, the businessman announced that he had an acute form of leukaemia. Tinkov transferred his stake in the bank to a family trust, and awaits a hearing about his U.S. extradition.

- By September, everything was aligned for Yandex to buy a bank, and for Tinkov to cash in on an asset that had soared in value. Yandex announced Tuesday a preliminary agreement to buy the bank for $5.5 billion, sending its shares soaring 13.6 percent.

- Whether by accident or design, Yandex’s announcement upstaged Sberbank’s planned party. The bank had earmarked Thursday for a grand unveiling of its transformation from a traditional — albeit enormous — bank into a fully-fledged tech company. To underline the change, the word ‘bank’ was cut from the company’s name and a new branding was commissioned from world-renowned agency Landor & FITCH.

- Sberbank CEO German Gref, a former government minister, is a big fan of visionary U.S. entrepreneurs in the Steve Jobs mould, and transforming his bank into a tech giant is the fulfillment of a long-held dream. Gref tried to hold an event like the spectacular product launches usually associated with Apple or Elon Musk, but didn’t quite hit the mark. Instead, Sber’s 30-minute video presentation, which was packed with expensive 3D graphics, resembled an extended commercial with amateur actors. Much of it was made up of Sberbank executives describing the company’s new services to ageing Russian celebrities like Soviet movie star Mikhail Boyarsky and pop star Dima Bilan.

- The re-branding was widely mocked by journalists and ad agencies alike. But, as one respected business journalist pointed out, Sberbank’s approach is different from many other large, state-owned Russian companies: it is trying to sell itself. This was far from a traditional pitch delivered in the manner of an annual report to the president.

Why the world should care

Yandex’s purchase of Tinkoff Bank gives the internet giant the necessary financial heft to challenge Sberbank’s plans to create Russia’s leading online ecosystem. The battle between the two companies in the coming years will be extremely interesting to watch.

Russia readies for a second wave of the pandemic

The Russian authorities U-turned this week. Since President Vladimir Putin’s announcement that COVID-19 was defeated, most officials have refused to recognize the danger of a second wave. But Moscow’s mayor this week began laying the ground for a new lockdown.

- Putin announced that the virus was defeated at the end of June — and most restrictions on movement and economic activity were lifted even earlier. Since then, the numbers of new infections and deaths have remained consistently low, although statistical analysis suggests these numbers are heavily massaged.

- From the middle of September, the number of daily new cases in Moscow — which had hovered at about 500 for months — began to grow. At first, the city authorities said this was down to increased testing, but journalists established that the number of tests was actually going down. The number of new cases in Moscow jumped Thursday to over 1,000 for the first time in three months, and the authorities abruptly changed course. Moscow Mayor Sergei Sobyanin urged companies to return staff to remote working, and re-introduced self-isolation for the over-65s and those with chronic illnesses. In the spring, these measures were a prelude to the implementation of a permit system for anyone wishing to leave their homes.

- At the moment, a return of such strict measures are not on the drawing board, according to sources at City Hall (but you should remember that plans for lockdown earlier this year were developed in secret). It’s particularly difficult to predict how the situation will develop because of the unreliability of the official figures about the spread of the virus.

- Any new lockdown will be especially hard on business. Most state support measures – deferred payments on tax bills and loans, a moratorium on bankruptcies, etc – were introduced in March for a six-month period. That means they expire this month. Trade associations have already written to the government to request an extension, but the response was not encouraging. Over the last couple of days, the Moscow authorities have shut down 49 shops for failing to observe coronavirus safety measures.

Why the world should care

Sobyanin was a key figure in Russia’s coronavirus response earlier this year and — as the official data is not trustworthy — the tightening of restrictions in Moscow is the best sign yet that a second wave is already underway.

Putin’s new economic policy

Looking closely at Russia’s three year budget — that was approved earlier this month — reveals a new sort of economic policy. Not only will the government play a drastically bigger role in resource redistribution, but higher taxes on big business, the wealthy and the upper middle class will pay for more financial support for Russians on low incomes.

- The 2021-23 budget anticipates a 10 percent cut in spending for the first time in four years, hitting almost every sector except state media. But that isn’t enough to cover the additional 4 trillion rubles ($52 billion) spent in 2020 to combat the pandemic and deal with falling oil prices. So, the government has adopted a benign sounding ‘revenue mobilization program’ to generate at least $20 billion a year from new taxes.

- Two categories of taxpayer will face the biggest bills — big business and high net worth individuals. Oil companies will lose some subsidies and face an annual tax hike worth about $5 billion, while the chemical and metals sectors will see extraction taxes rocket more than threefold. Individuals with an annual taxable income in excess of 5 million rubles ($65,000) will see their income tax bill go up two percentage points to 15 percent, while interest on bank accounts with more than 1 million rubles ($15,000) will also see higher taxes. Entrepreneurs working in offshore jurisdictions like Cyprus will face a sharp increase in dividend tax — from 0.5 percent to 15 percent. And, finally, the state will impose the biggest ever rise in excise duty on cigarettes — up by 20 percent.

- The biggest beneficiaries of these measures should be small and medium-sized businesses and Russians on low incomes. We calculated earlier this year that it was these sectors that received the most money from the government’s anti-crisis program. But officials — from Putin downwards — have made it clear that this is not a one-off: tax reductions for small and medium-sized businesses will be permanent.

- Taken together, all these measures amount to a new form of economic policy. Much of it seems to be a response to leading Kremlin ideologue Vyacheslav Volodin, the current parliament speaker. His call for “social justice” first appeared in 2019 as part of a program that paved the way for the constitutional reforms that ‘reset’ Putin’s term count, allowing him to rule through 2036.

- But other influential officials have been talking about similar ideas. Earlier this month, we saw a raft of proposals to help the poor: ex-Prime Minister Dmitry Medvedev suggested a Universal Basic Income, and senior banker Andrei Kostin proposed a “negative income tax” for those earning the least. This week, the government implemented new rules for calculating the minimum wage, a long overdue overhaul of a system unchanged since 1997. This will help address income inequality but will take $6 billion a year from the budget by 2025. That list of new taxes on the rich may not be finished just yet.

- State media have presented the new measures as a tax on oligarchs and rich Russians who syphon their funds offshore. That’s partly true, but it’s not the whole story. For example, a tax on bank deposits worth 1 million rubles or more would affect 55 per cent of all bank accounts in the country (a million rubles is a relatively normal level of savings for someone who enjoys a good pension).

Why the world should care

The raft of recent tax hikes and legislative changes amount to something more than just crisis management — the Russian government looks like it is radically re-thinking how it approaches economic policy and the redistribution of wealth.

{kind=link}