THE BELL WEEKLY: Sabotage claims fuel nationalization drive

Hello! This week our main story is Vladimir Putin letting some Western investors sell their frozen Russian assets ahead of his high-stakes call with Donald Trump. We also look at what Russians stand to lose if Radio Free Europe/Radio Liberty ceases to exist and take stock of mounting worries over the state of the Russian economy.

Ahead of Trump call, Putin lets Western funds sell frozen Russian assets for the first time

On the eve of a phone call with Donald Trump, Vladimir Putin unveiled his latest overture to the United States. For the first time in three years of war, he signed an order on Monday allowing major US investment funds to sell their holdings of frozen Russian securities. The move comes as US media report the White House is looking at what carrots it can offer Moscow, with the potential recognition of Crimea as Russian territory on the table.

- Vladimir Putin has signed an order allowing ten investment funds from the US and UK to sell their assets in Russia. From the list of firms, it is clear the assets in question are Russian securities, in which non-resident investors held large stakes before the war. On 1 February 2022, non-residents owned around 20% of Russian government bonds (OFZs). Among those given the green light to sell are some of the largest Western funds that have invested in Russia, including Franklin Templeton, GMO, Jane Street and Baillie Gifford.

- Putin's decision is a milestone: no Western investment fund has yet been able to pull out or sell securities stuck in Russia. They have not been nationalised, but the assets have been transferred to frozen so-called type-C escrow accounts, from which money cannot be withdrawn without permission from the Russian authorities. In total, these accounts had assets worth 500 billion rubles ($6.4 billion) in them as of March 2023, Bloomberg reported, citing Central Bank data.

- The buyer, listed in Putin's order, is little-known New York-based hedge fund 683 Capital Partners. But they won’t hold onto them for long. Putin has also authorised two Russian legal entities, LLC Cepheus-2 and LLC Sovremennye Fonds Nedvizhimosti, former structures of Sber, which are most likely still connected with the state bank, to buy the assets from 683 Capital Partners.

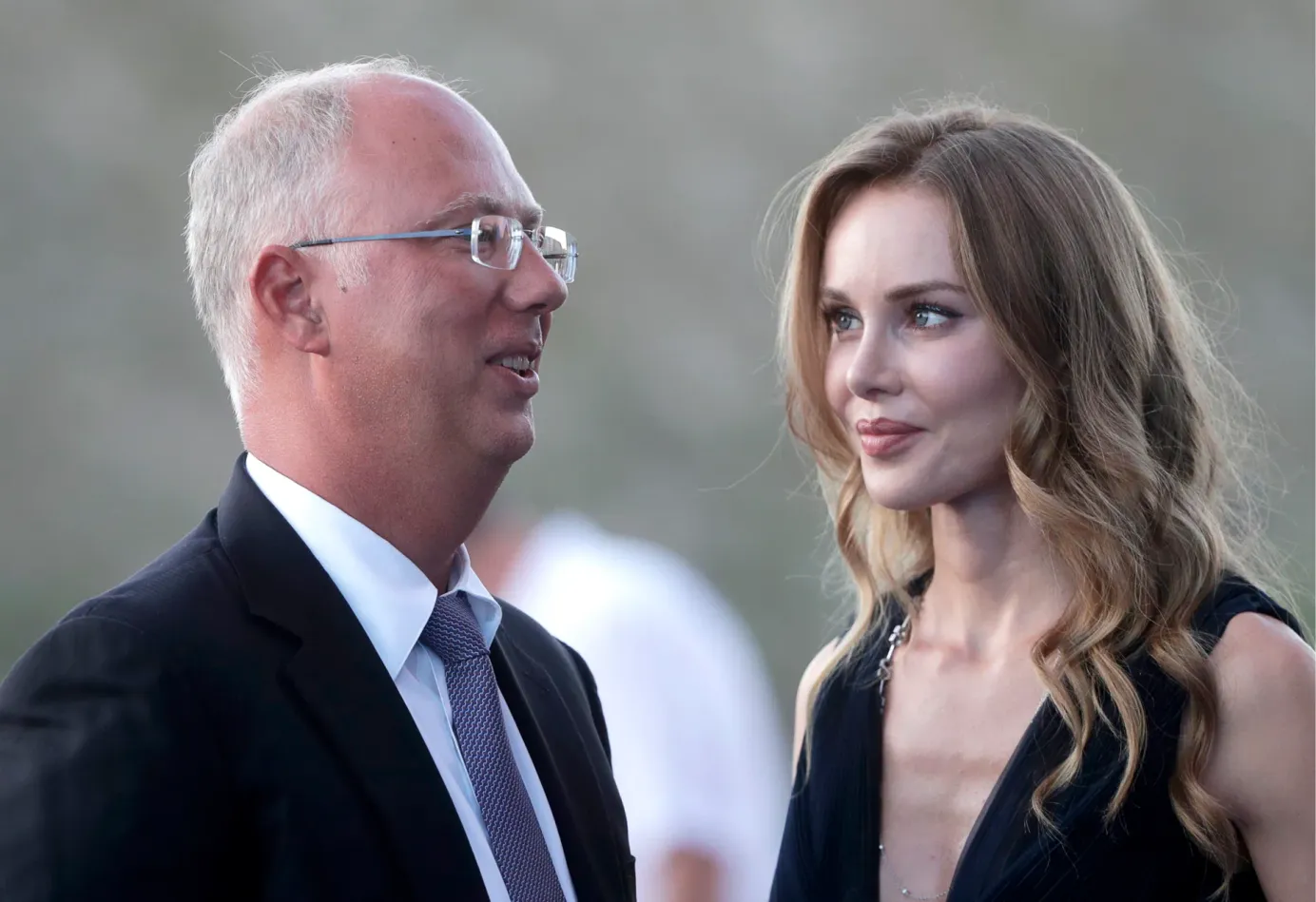

- Who is 683 Capital Partners and why are they involved as a middle-man in the deal? According to the US Securities and Exchange Commission, at the end of 2024, 683 Capital Partners managed assets worth $1.6bn (a tiny amount in the hedge fund world), and had just 10 employees. The firm seems to have nothing to do with Russia. But The Bell immediately noticed that the founder and head of the fund, Ari Zweiman, studied at both Stanford and Harvard in exactly the same years as the head of RDIF, Kirill Dmitriev, who is now one of the negotiators with the Americans, focused on economy issues. In response to a question about his possible association with Zweiman, Dmitriev said: "I am not familiar, neither I nor RDIF has ever had any contacts with this fund."

- The authorisation of these deals comes a day before a phone call between Putin and Trump, during which the two sides will discuss (1, 2) terms for ending the war in Ukraine. Trump himself said on Monday night that the conversation would take place in the morning (i.e. evening Moscow time). Semafor claimed that the White House is going through a variety of options on what to promise Vladimir Putin for agreeing to a ceasefire in Ukraine – including allegedly exploring the possibility of recognising Crimea as Russian.

Why the world should care

The scheme for selling the Russian assets of American investment funds described in Vladimir Putin's order looks suspicious. Western funds for some reason sell their assets to an intermediary who will then resell the securities to a Russian entity. There can only be two good explanations for such a scheme: protecting the Western sellers from the threat of sanctions, and kickbacks for the intermediary players (quite possibly both).

The end of Radio Liberty: What does it mean for Russia?

President Donald Trump’s decision to liquidate the U.S. Agency for Global Media and stop funding Radio Free Europe/Radio Liberty has had a particularly strong impact on Russian society – not least because of the important role RFE/RL played throughout Soviet/Russian history. If RFE/RL ceases its work, uncensored Russian journalism will lose a valuable institution.

- The Trump administration’s decision to halt federal grant funding to RFE/RL was always going to trigger a reaction in Russia. Those living in the Soviet Union and behind the Iron Curtain were the key target audience when the organization was created in the 1950s at the start of the Cold War. Alongside the BBC Russian Service, RFE/RL formed the basis of a phenomenon that was dubbed “enemy voices” in the Soviet era.

- From the 1960s to the 1980s, these radio stations were the main – and in many cases only – source of uncensored information about the outside world that got through to the Soviet Union. And it wasn’t just international news: Soviet citizens famously first heard of the 1986 Chernobyl nuclear disaster from Radio Liberty and the BBC. The Soviet authorities understood the danger posed by these “enemy voices”: Western radio stations were jammed using special equipment and were often targeted by the Soviet press.

- Radio Liberty was also a significant cultural player in Soviet times. Almost every major exiled Russian writer or poet worked for the station: Gaito Gazdanov, Alexander Galich, Sergei Dovlatov, Viktor Nekrasov, Vladimir Voinovich and many more. The outlet played an important role in preserving Russian culture that the authorities had banned, and provided a valuable source of income for émigré writers in the West.

- After the fall of the USSR and the end of the Cold War, the Russian editorial staff at Radio Liberty faced an obvious and long-term crisis. It came to be seen as a cosy “retirement home” for veteran journalists to wind down their careers. That changed in the 2010s, as Russia's own media faced increased censorship, RFE/RL’s work took on renewed meaning and it rejoined the ranks of significant Russian-language independent media media. Like the Soviet authorities before them, the Kremlin also started paying closer attention. Radio Liberty was deemed a “foreign agent” as early as 2020, long before many other media outlets.

- Radio broadcasts have lost their prominence in the internet age, but the Russian language output at Radio Liberty has remained one of the most high-profile independent sources of news and reporting. They conduct high quality investigative journalism and its journalists are among the leading Russian OSINT experts. Its Current Time TV station – co-produced with Voice of America – stands alongside TV Dozhd as the only fully-fledged Russian-language independent/opposition TV broadcasters. In addition, Radio Liberty is one of the few outlets that can produce almost academic-standard shows about Russian culture.

- This illustrious history appears to be coming to an end. According to unverified reports, RFE/RL’s Russian staff have already been told that the media organization is finished and that all employees will be dismissed over the next two weeks.

Why the world should care

If the American authorities had shut down Radio Liberty in 1995, or even 2005, few in Russia would have noticed. But closing RFE/RL now, when the organization is relevant once again and its work is in demand, seems highly short-sighted.

Does Russia really face a wave of bankruptcies

Amid the central bank’s aggressive interest rate hikes last year – taking the key rate to a two-decade high of 21% – the industrial lobby, joined by sympathetic economists, has been increasingly warning of a wave of bankruptcies as over-exposed industries struggle to service their debts. We took a look at how bad things really are.

- “The Russian economy faces the threat of a large-scale surge in corporate bankruptcies,” the Center for Macroeconomic Analysis and Short-term Forecasts (CMASF) wrote in its January report. CMASF was founded by current Defense Minister Andrei Belousov and is now headed by his brother Dmitry. Even such respected individuals as Sergei Chemezov, head of state defense corporation Rostec, and Russia’s wealthiest man Alexei Mordashov are complaining about the difficulties of servicing their debts. The government set up a special commission under deputy PM Alexander Novak to discuss state support for troubled industries.

- Objective indicators support the lobbyists’ concerns. At the end of 2024, over 20% of companies in the manufacturing sector were paying more than two-thirds of their pre-tax profits on debt repayments — double the number of firms as in 2023.

- Industries which saw the most intense overheating and those worst affected by sanctions are now facing the biggest problems.

- The coal industry is in first place: last year, more than half of companies were unprofitable. It was the only sector in Russia to post a combined loss for 2024. As in the 1990s, woes in the mining sector risk becoming a social problem. In December, miners at one pit in the Kemerovo region declared a hunger and labour strike. The main issues facing the industry are low global prices due to falling demand, sanctions, and increased railway tariffs.

- According to CMASF, the companies in the most difficult position are those at the “technological core of the economy”, with transport and engineering in the worst situation. For example, the authorities constantly have to subsidize auto maker AvtoVAZ, which has debts of more than 100 billion rubles. “With the increase in the base rate, payments to banks are up by billions of rubles a year,” complained Chemezov (his Rostec owns a 32.3% stake in the company). But defense and related industries are a separate case. Businesses in the military-industrial sector are among the main recipients of preferential loans. Moreover, the general economic cooling will have less of an impact on them since demand for military equipment comes from the state and this will be sustained, even if the war ends tomorrow.

- Any problems in the economy are inevitably accompanied by discussions about the state of the real estate market. This time, though, developers face a unique situation: the rapid rise in interest rates coincided with the end of a trillion-ruble preferential mortgage program in the summer of 2024. That program had supported the industry since 2020. In the first half of 2024, 80% of all newbuild apartments were sold with a preferential mortgage. After the biggest of these schemes were cancelled, the market for new homes collapsed in the second half of the year. Deputy PM Marat Khusnullin, who is responsible for the industry, allowed isolated bankruptcies to take place. “Some developers miscalculated their economics, they probably won’t cope,” he said. But in general, experts in the sector are in no rush to sound the alarm. Sales of housing commissioned and under construction in 2025 remain high.

- Another candidate for serial bankruptcies is the freight transport sector. High costs for borrowing and leasing, increased recycling fees for imported equipment, higher prices on fuel and vehicle servicing and a fall in demand could push about 30% of freight carriers into bankruptcy in 2025.

- Retail trade is one of the most heavily indebted (.xlsx) sectors of Russia’s economy. High interest rates and the subsequent increase in the cost of borrowing can affect many different industries. First and foremost, the auto market, which became predominantly Chinese after the exodus of Western brands. Even without high interest rates, the profitability of selling cars from China in Russia is very low. Shopping malls have also faced heightened risks. Last year, the Union of Russian Shopping Malls warned that high interest rates and poor performance in competition with online marketplaces could drive a quarter of shopping centers into bankruptcy.

How real is this threat?

Despite debt problems in a whole range of sectors, talk of a full-blown crisis is premature, according to experts who spoke with The Bell.

Economist Sergei Skatov noted that the banks – who have the most accurate information about borrowers – are not anticipating a wave of bankruptcies. If they were worried about this development, lenders would have needed to establish additional reserves last year to cover bad debts. However, according to Central Bank figures, this didn’t happen.

Overdue payments on corporate loans remain (.xlsx) at their lowest level since mid-2021 – 2.7 trillion rubles. Due to the rapid expansion of the loan portfolio, any problems with new debts are not immediately apparent. “But even allowing for the effect of this rapid growth, the overall economic situation does not lend itself to alarmist forecasts,” Skatov reassured.

Bankruptcy is not the usual solution to problems in the Russian economy, Skatov said. The state more often bails out troubled companies with an injection of money. In previous crises, both businesses and banks happily took advantage of this.

Why the world should care

Under pressure from high interest rates – which nobody is planning to lower just yet – and sanctions, Russia’s economic situation is deteriorating. But it’s still a long way from total collapse.

PAID SUBSCRIPTION LAUNCH

From May 1, 2025, The Bell in English will no longer be free

From May 1, 2025, all The Bell’s newsletters and online content will be behind a paywall. We have taken this decision so that The Bell can remain financially independent, and maintain our high standards of journalism and economic expertise

Exclusive analysis of Russian economics and politics

Exclusive analysis of Russian economics and politics

{kind=link}