The collapsing ruble is a headache for the Kremlin

Hello! This is your weekly guide to the Russian economy — prepared and brought to you by The Bell. In this newsletter we focus on why the Russian currency is on a rollercoaster and what political consequences it may have. We also look at how the government might be able to make spending cuts.

Dear readers,

We’re very grateful for your support (you can donate here!). But we’d love to hear more about how we can further develop The Bell’s English-language service. We think the best way to understand what you want is to talk face-to-face. If you can space half-an-hour for a Zoom call, drop an email to our editor at p.mironenko@thebell.io and we’ll get in touch. Thanks!

How ruble weakness affects the country’s finances

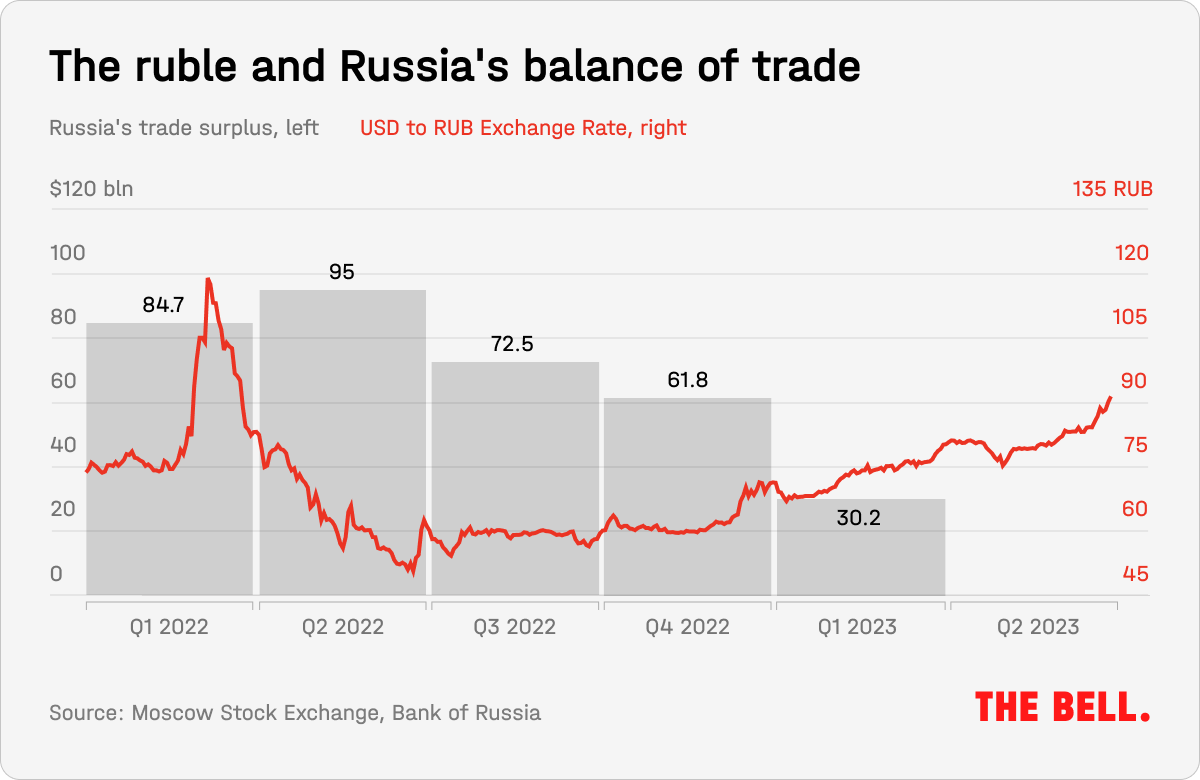

The Russian currency has been tumbling all week. The rate against the U.S. dollar dropped as low as 94 rubles on Thursday, while against the euro it fell to 102. This is the weakest the ruble has been since March 2022 when it collapsed in the wake of Russia’s invasion of Ukraine. The ruble has lost about a third of its value since the start of the year and is — so far — this year’s worst performing emerging market currency.

What’s going on?

Yevgeny Prigozhin’s insurrection last month was the immediate trigger for the currency’s current weakness. The mercenary leader’s short-lived uprising meant people again began factoring in the risk of domestic political instability to the value of the ruble. It’s the first time since opposition protests in 2011 and 2012 that domestic politics has led to serious fluctuations in the price of the ruble.

However, there are also underlying issues. Everything is stacked against the ruble at the moment: low exports, increased imports, the ongoing transfer of funds out of Russia to accounts abroad, extremely low liquidity levels and the absence of non-residents in the currency markets.

The final point is particularly significant. In previous years, a serious devaluation of the ruble attracted non-residents looking to capitalize on the differences between interest rates and exchange rates. Today, they are gone — and Western sanctions, Russia’s isolation and the war in Ukraine mean they won’t be coming back.

As a result, the ruble exchange rate is far more dependent on Russia’s balance of trade. That’s what Central Bank deputy head Ksenia Yudayeva identified as the key factor behind the current slump. “We are seeing a significant reduction in the current account this year, when compared with last year and the last quarter. Among other things, this is due to a decrease in export earnings and, in my opinion, falling prices,” she said Tuesday.

Central Bank head Elvira Nabiullina also said the changes to the balance of trade (a drop in the difference between exports and imports) was the main reason for the ruble’s weakness.

The ruble’s collapse coincided with an unexpected midnight meeting between Russian President Vladimir Putin and Prime Minister Mikhail Mishustin that extended into the early hours of Wednesday morning. It’s not known whether the ruble was discussed and there is no word of it in the published account of the meeting. However, the economic successes that Mishustin reported to Putin (and which are in the published account) are yet more reasons for the ruble’s fall — they include an increase in real incomes, record low unemployment and growing demand among consumers and wholesalers.

What does it mean for the Russian government?

One school of thought suggests that the ruble’s devaluation is good for officials as it means the country acquires more rubles for the same amount of raw material exports. This idea dates back to the late 1990s when revenue was directly linked to oil prices — but it is much less relevant today. Now, revenues are prescribed in advance and the link to fluctuating oil prices (and, thus, fluctuating exchange rates) is counterbalanced by self-imposed rules obliging the Finance Ministry to buy or sell foreign currency reserves (according to the export price for oil). As a result, exchange rate fluctuations are not reflected in the budget.

Moreover, the old belief that a falling exchange rate boosts revenues is greatly undermined when the government is financing expenditure by borrowing on the markets. The Finance Ministry last year issued 3.3 trillion rubles’ worth of bonds (almost $50 billion) and plans to do the same this year. The ruble’s collapse leads to faster inflation and, as a result, higher interest rates — making borrowing more expensive.

Of course, exporters who are paid in foreign currency and spend in rubles will benefit from the falling ruble. Part of their profits will, however, be collected as tax — but that will come later. Those exporters who are in no hurry to return foreign earnings to Russia could be the ones who ultimately stabilize the exchange rate. In previous moments of crisis, it appears that exporters have received urgent requests to buy rubles from the Kremlin.

It's unlikely the Central Bank will intervene to prop up the ruble. Since 2014, the regulator has preferred to fight inflation by adjusting interest rates. Central Bank officials never tire of repeating the mantra that exchange rates are determined by supply and demand, and that any ruble rate is acceptable to them. We heard such a statement again this week.

In theory, nothing prevents the Central Bank from making a currency intervention if it fears a threat to the stability of the financial system. For example, immediately after the invasion of Ukraine last year, the Central Bank sold 100 billion rubles’ worth of foreign currency. However, the regulator has said that it currently sees no threat to the stability of the system. That means there won’t be any intervention — at least, not yet.

Why the world should care

As always, a falling ruble will drive up prices for imported goods in Russia, especially those that the country does not produce (from smartphones and laptops to rum and whisky). Prices are likely to rise faster for goods arriving in Russia as “parallel imports” — a scheme introduced after Western sanctions that allows importers to bring in goods to Russia that were not originally intended for the country.

However, the falling ruble will affect prices across the board in Russia. While earlier devaluations incentivized domestic productivity and import substitution, the shortage of labor and capacity might prevent a repeat of such an effect this time around.

Another potential consequence is a jump in inflation and a decision at the Central Bank meeting on July 21 to raise rates. Finally, it also appears inevitable that sharp fluctuations in the value of the ruble will now become routine.

How will Russia make budget cuts?

The Finance Ministry is proposing major cuts in government spending in next year’s budget, with each ministry to reduce expenses by 10%. The reasoning is clear: the budget deficit is growing. A government commission on budget projections discussed the issue at a meeting last week. Increased borrowing was mooted as an alternative to cutting costs, but this was reportedly strongly opposed by Central Bank officials.

Past crises in Russia have also led to spending cuts. In 2018, pension provision went under the knife via a decrease in transfers to the pension fund (there are not anticipated to be any increases in revenues for the pension fund this year, nor an increase in insurance premiums). Back then, defense spending also faced cutbacks (but this is obviously not happening in 2023). It remains unclear how the Finance Ministry will cut expenditures, but calls to cut costs are a traditional opening gambit in the process of negotiating the budget.

Key figures

Central Bank figures for April continue to show household funds flowing into deposits abroad — or into cash. There’s been little sign of this trend changing in May and June — something that has put extra pressure on the ruble.

Nabiullina said that the Central Bank still believes its monetary policy to be effective. The policy, which includes a floating exchange rate and inflation targeting, remains unchanged despite the weakening ruble.

The State Statistics Service (Rosstat) released figures about GDP by usage in the first quarter of this year. State orders reached a historic high of 24.7% of GDP, which will be no surprise to most. Exports were down 5.5 percentage points — however, it’s impossible to reliably estimate real imports and exports as Russia no longer publishes trade data.

Inflation is up for the second week running. The consumer price index from June 27 to July 3 rose 0.13% compared with the previous week. And that’s despite the fact that the usual July increase in utility payments did not happen — they were indexed back in December. Annual inflation moved up from 3.2% to 3.3% over the course of the last week.

What to watch next week

- Q2 balance of payments (Central Bank, 11 July)

- “Talking Trends” report (Central Bank, 12 July)

- June Consumer Price Index (Rosstat, 12 July)

- Weekly inflation (Rosstat, 12 July)

{kind=link}