How Russia's economy survived two years of war

Hello! Welcome to your weekly guide to the Russian economy — written by Alexandra Prokopenko, Alexander Kolyandr and Denis Kasyanchuk and brought to you by The Bell. To mark the second anniversary of Russia’s full-scale invasion of Ukraine, we take an in depth look at how Russia’s economy has survived and adapted in wartime.

Russia’s militarized economy is storing up problems for the future

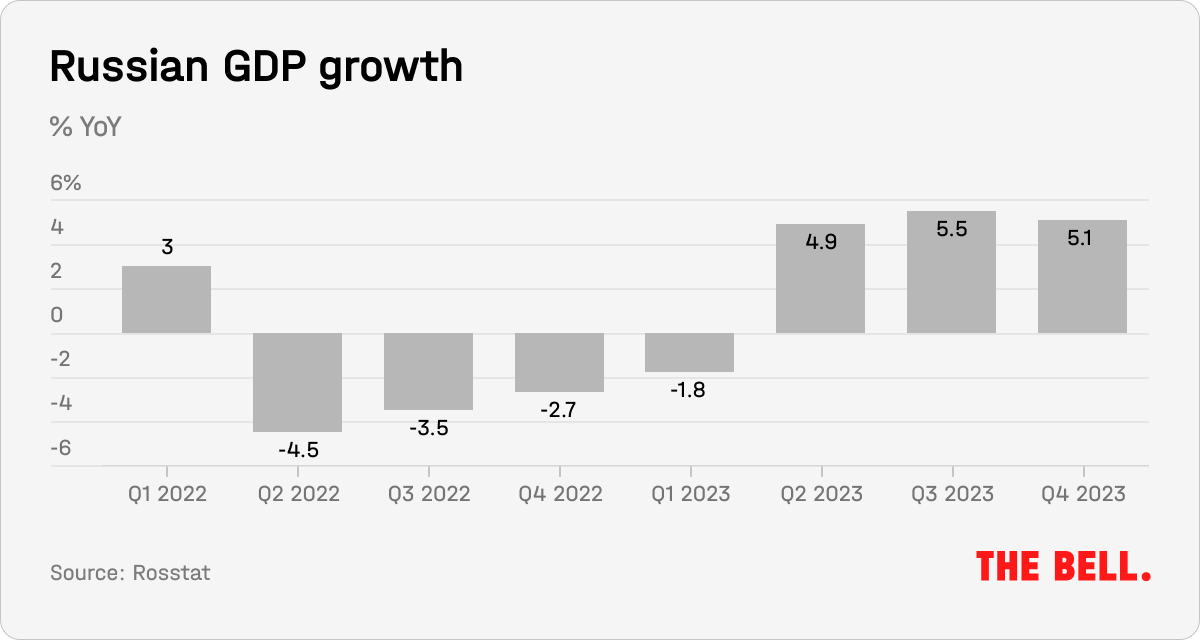

Russia's economy has demonstrated both resilience in the face of Western sanctions, and flexibility in restructuring trading relationships and domestic demand. Since the Kremlin sent tanks across the border into Ukraine in 2022, China has replaced the European Union as Russia's primary trading partner and tech supplier, while, domestically, the increase in military spending has given a major stimulus to the broader economy.

Superficially, military spending and buoyant revenues from hydrocarbons mean the Russian economy can appear to be flourishing. But this is not a healthy sort of flourishing, and economic growth is masking a decline in productivity, rising currency instability, fiscal difficulties, labor shortages and a reversion to less sophisticated technologies.

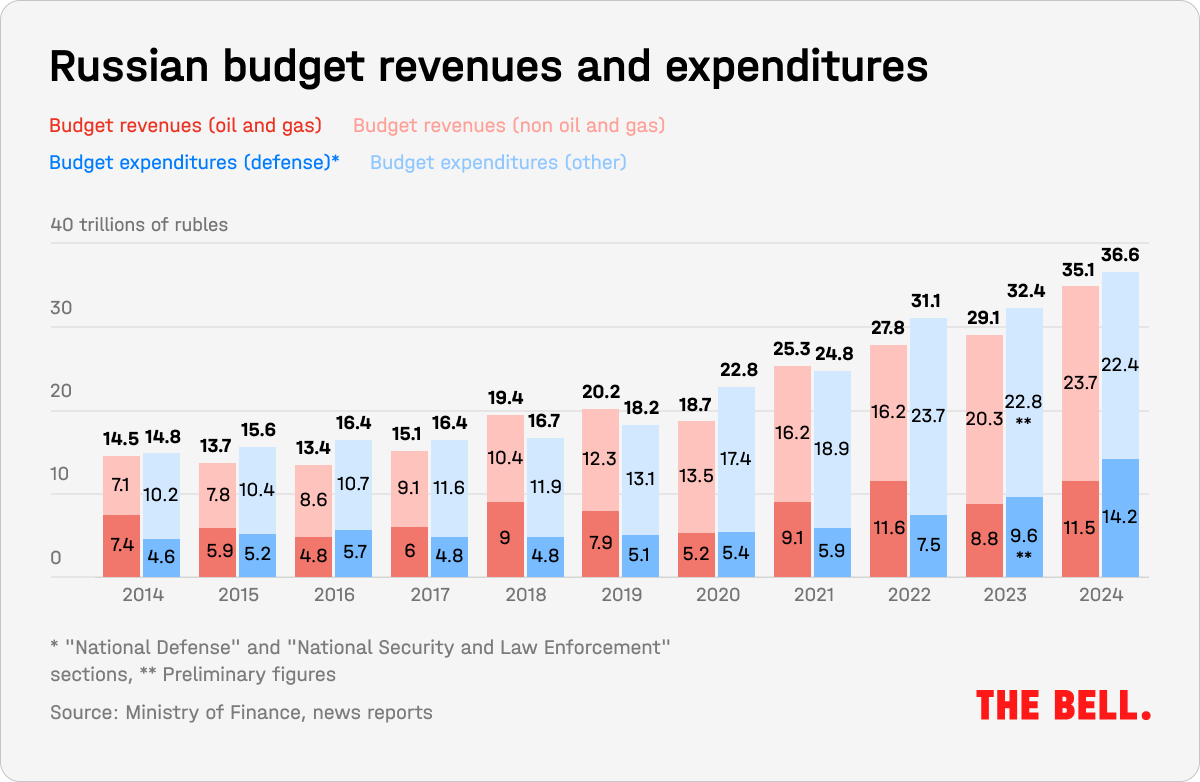

Budget: there’s still money to pay for the war

President Vladimir Putin has committed record sums to Russia’s war in Ukraine: in 2022 and 2023, spending topped 30 trillion rubles. Five years ago it was half that size.

In this way, the Russian authorities have changed how demand is distributed in the economy. Now, the greatest demand comes from an expanded defense sector. As in Soviet times, the war has been a financial boon for the military-industrial complex and related industries, the armed forces and their families, and all parts of the public sector that are connected with defense and security.

High levels of public spending, which also includes preferential loans, prompted the Central Bank to hike interest rates to 16%. It also drives inflation.

It’s more than likely that these trends will continue through 2024, and we will see the level of military and national security spending exceed 8% of GDP for the first time in history. Alongside oil revenues, Russia’s economic fortunes are now tied to the military and the defense industry. We looked in detail at the consequences of this here.

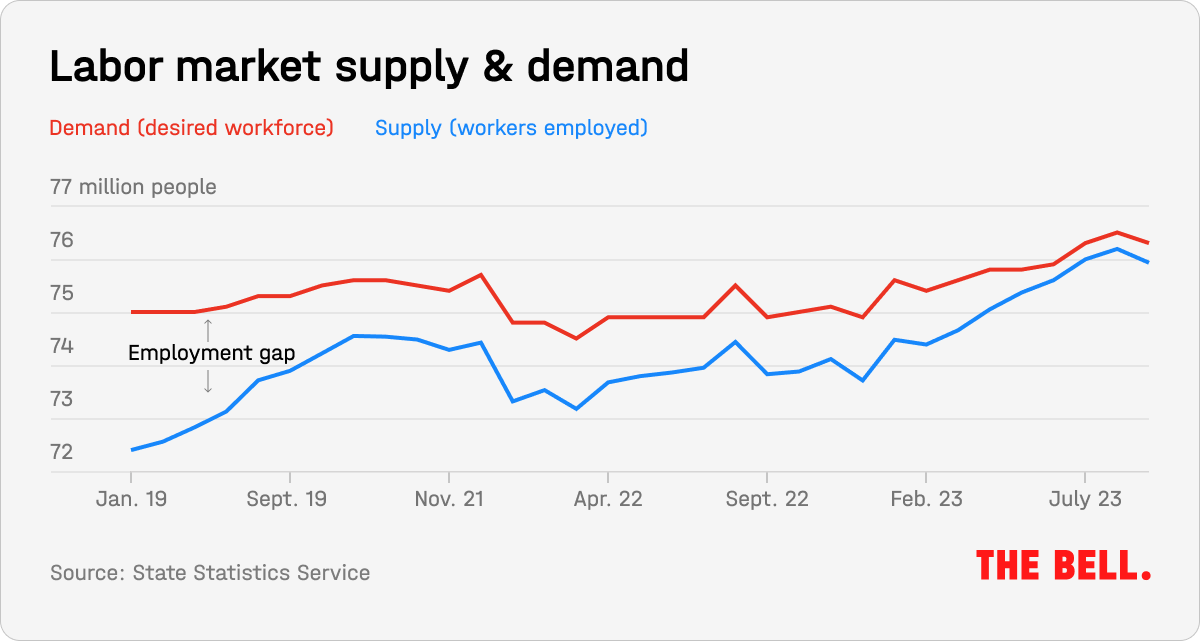

Labor market: nobody to hire

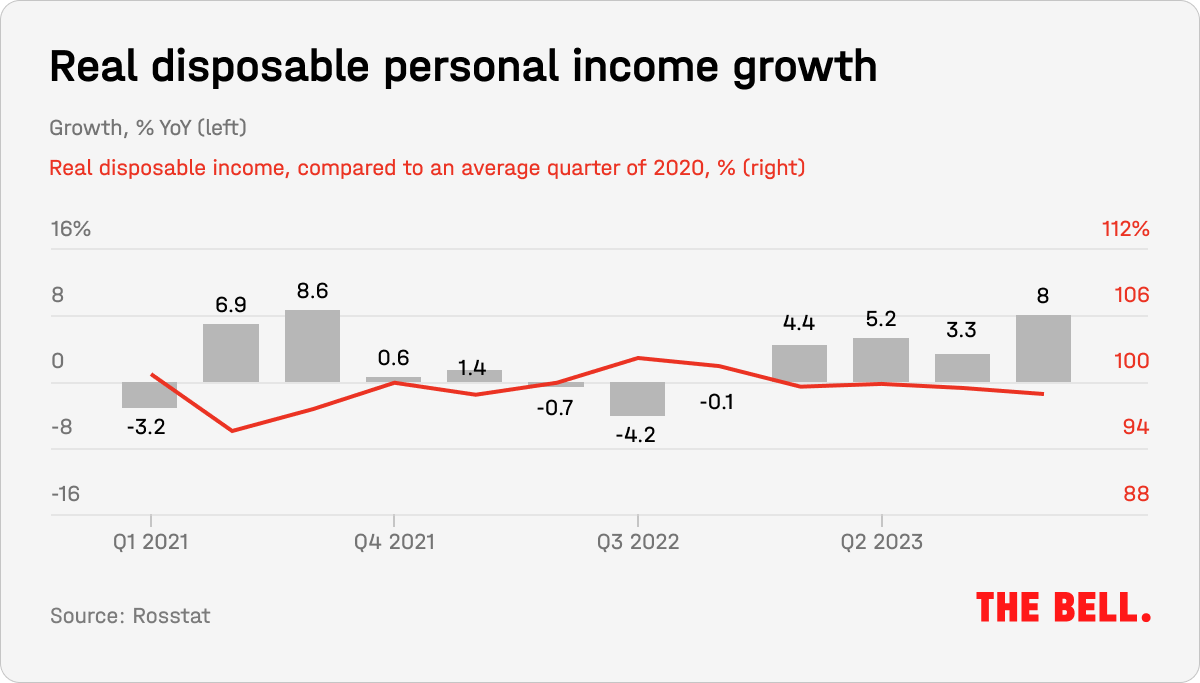

The militarization of the economy has been the primary driver of rising demand on the labor market. And this rise was accompanied by a decline in supply as hundreds of thousands of able-bodied Russians went to the front, or fled the country. As a result, Russia is experiencing a labor shortage. This benefits workers, who can command higher salaries. As a result, real wages and disposable incomes in Russia are on the rise.

However, this growth is relative as it follows a significant fall in 2022. In fact, real wages and disposable incomes have only just rebounded to 2020 levels.

In addition, high demand for workers and the difficulties of accessing Western technology means Russia saw a record 3.6% fall in labor productivity in 2023 (second only in this century to the 4.1% fall recorded in 2009 amid the global economic crisis). Over the last two years, the average Russian has been earning more and producing less.

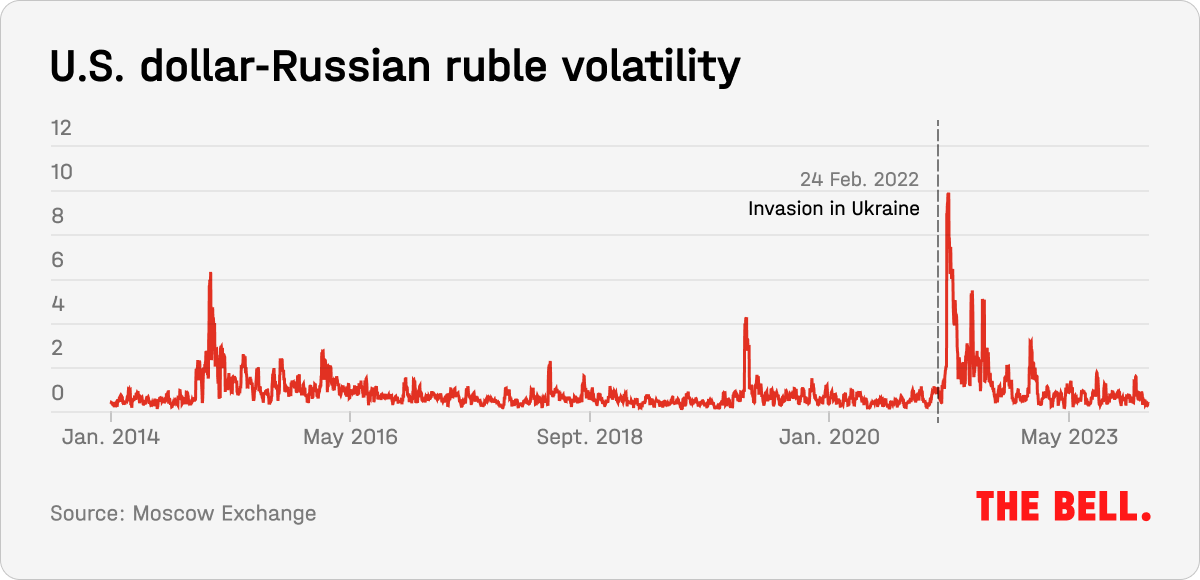

The ruble: unprecedented volatility

A widely fluctuating exchange rate has become the new normal. At different points over the last two years, you could buy a U.S. dollar for 50 rubles, and also for 100 rubles. After the abolition of Russia’s “budget rules,” the exchange rate has been determined solely by trade flows. As a result, in summer 2023, when export revenues hit a ceiling and demand for imports continued to rise, the ruble collapsed to 100 rubles against the U.S. dollar.

In an attempt to exert control, the authorities forced exporters to sell foreign currency earnings. Strictly speaking, neither the government, nor the Central Bank, has an exchange rate target, so it is wrong to talk about abandoning a floating ruble. Equally, though, it is incorrect to assume that the current rate is entirely market based.

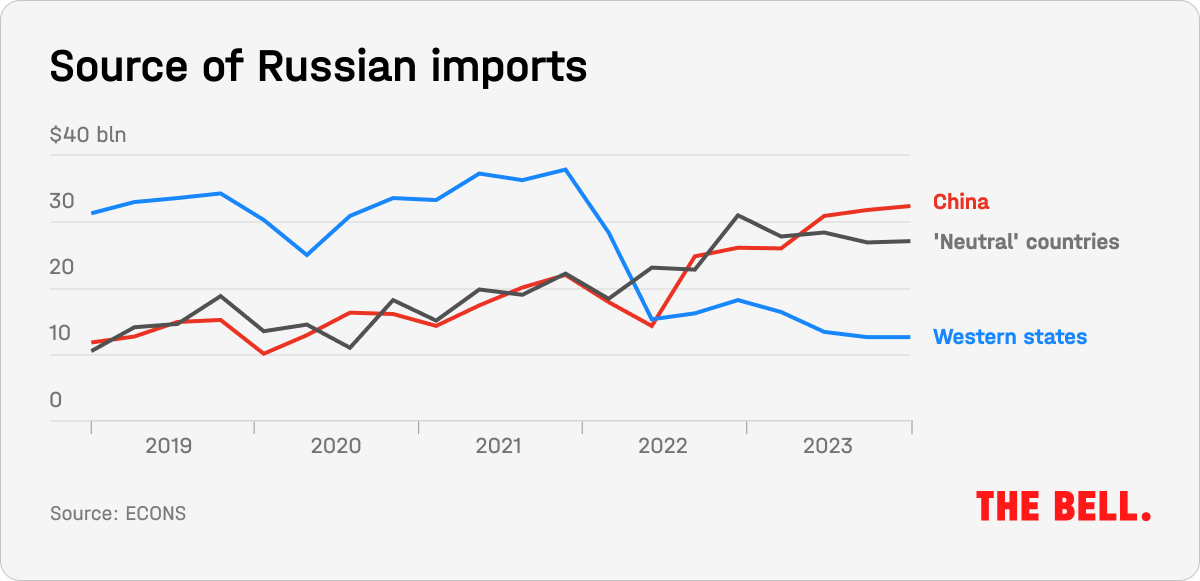

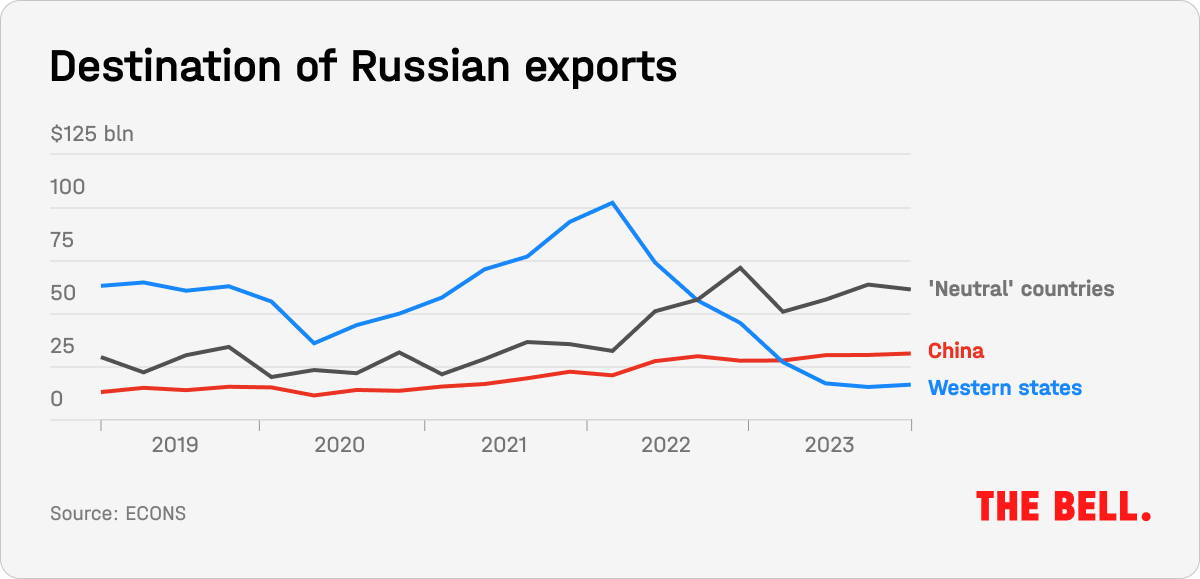

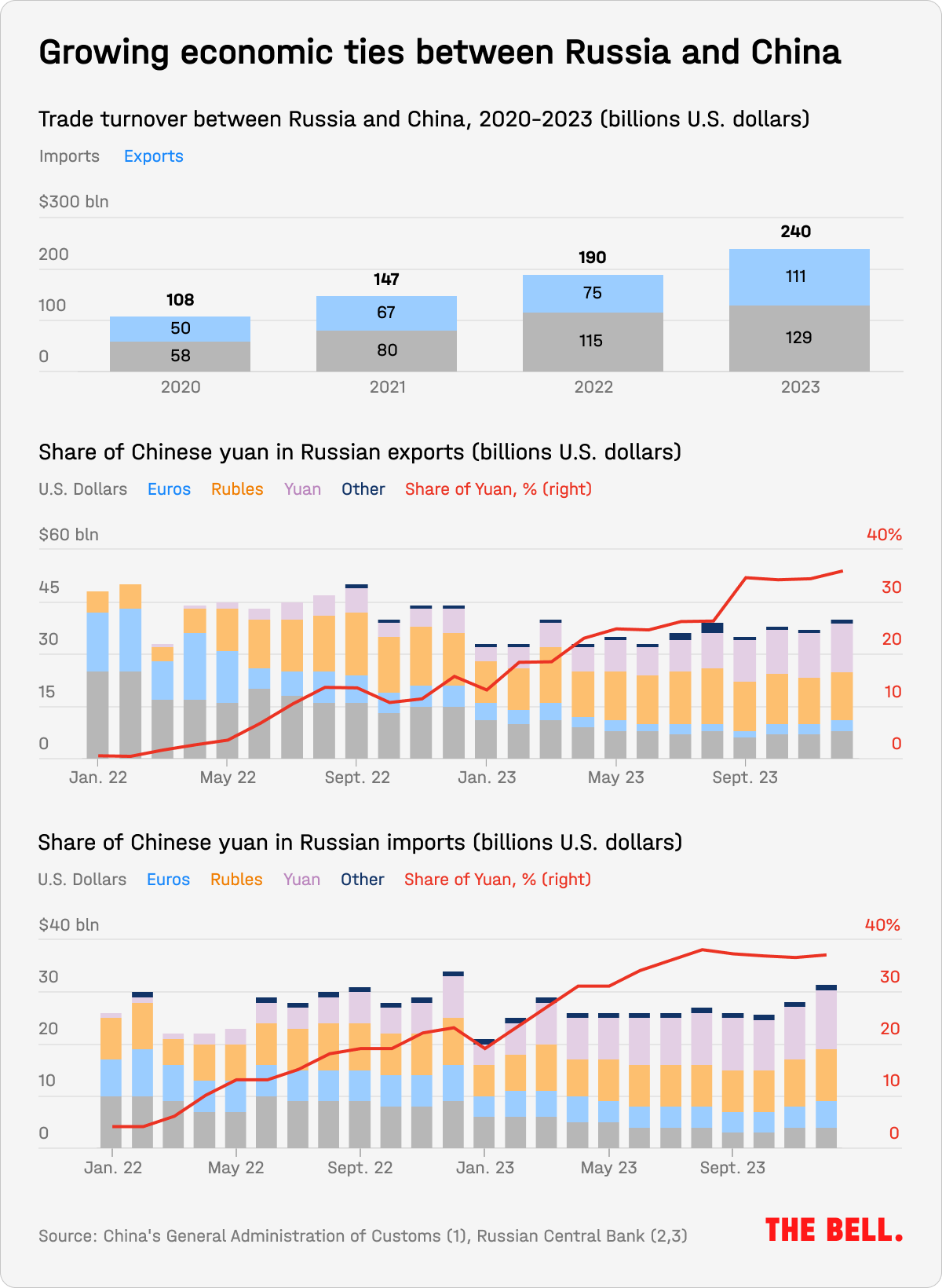

International trade: replacing Europe with China and the Global South

Over the last two years, Russian foreign trade has undergone changes that are comparable in their scale with those seen in the 1990s. We’ve seen a transformation of both logistics, and the geography of imports and exports. This is clearly illustrated by two graphs published by economic research outlet Econs.

Technological and financial sanctions imposed by the West at the start of the war obliged Russia to replace imports from the EU and other developed countries. The main source of imports has shifted from Europe to China, which now provides 45% of Russia’s imports (up from 27% before the war). Developed economies dropped from providing 47% of Russian imports to just 17%. However, import substitution has not been total. Parts and components now make up a smaller proportion of overall imports and this implies a decline in localized production – instead of assembling cars, for example, Russia is back to purchasing ready-made ones.

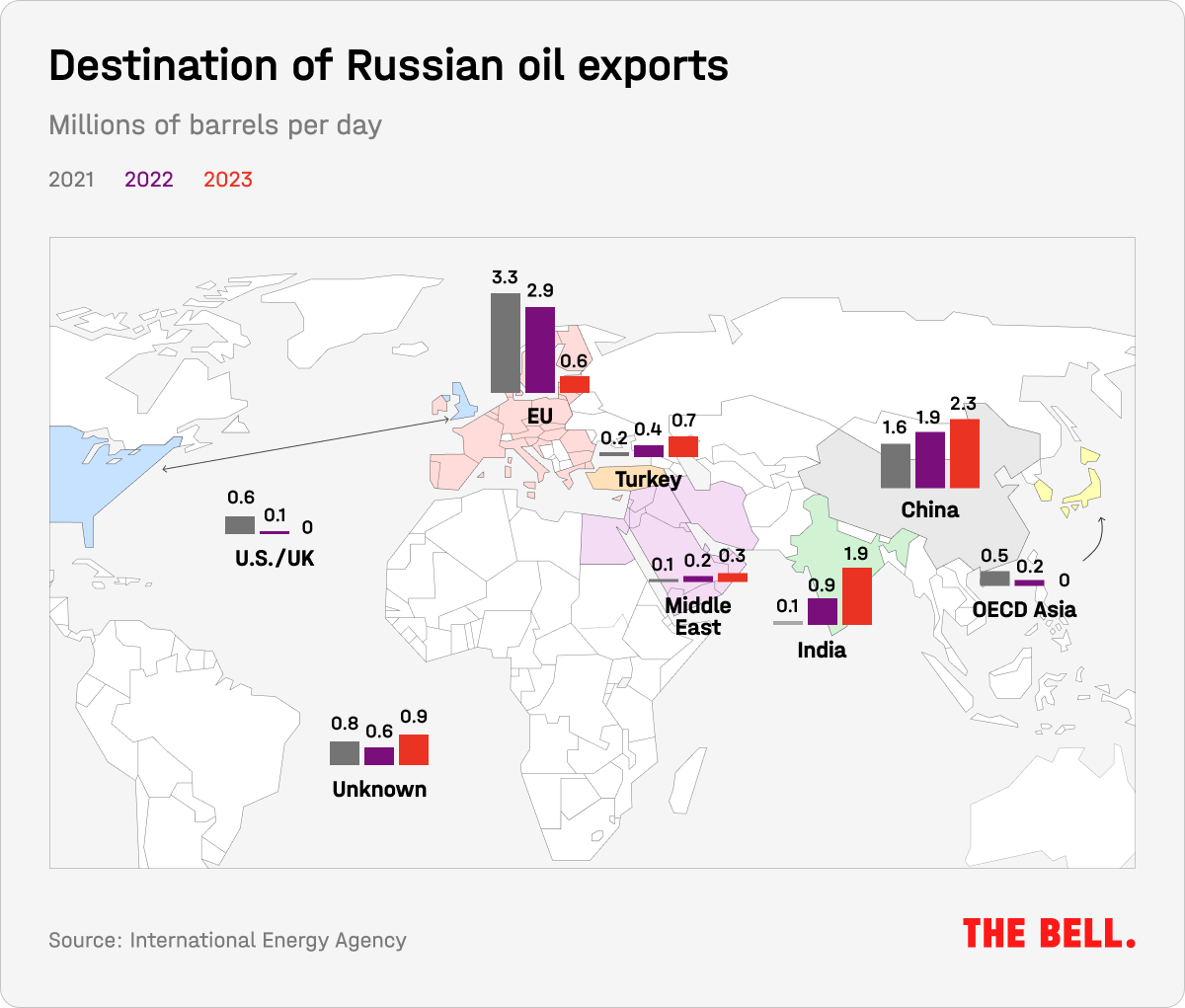

Russia’s raw material exports have responded well to the loss of Western markets, and have been quickly diverted to other countries.

Replacing the U.S. dollar with the Chinese yuan

Conflict with the west has forced Russia into China's embrace (we recently discussed this in detail here). In just two years, trade in the yuan on the Moscow Exchange went from almost nothing to nearly a third of the market. In December, 35.8% of Russia’s exports were purchased in yuan, along with 37% of imports. At the same time, exports in foreign currencies reached their highest level since January 2022 ($2.8 billion of the total $5.4 billion was settled in yuan). In 2023, $68.7 billion was held in yuan in Russian bank accounts, compared with $64.7 billion in dollars. Lending to companies in yuan was up 3.6 times to $46.1 billion in 2023, largely due to the conversion of debt from dollars and euros.

Although a substantial part of Russia’s banking sector is under Western sanctions, a chunk of export-import payments still happen in U.S. dollars and euros. However, after U.S. President Joe Biden's decree on secondary sanctions, Russian businesses have increasingly encountered problems with transactions in “friendly” countries such as Turkey, the UAE and China. This means that the yuan will be used even more.

Why the world should care

Amid the war in Ukraine, the Kremlin has managed to continue to acquire essential chips and semiconductors via third countries, and it has successfully switched its oil exports to Asian buyers. However, the current stability is not likely to endure: in 1-2 years, the structure will begin to wobble due to accumulated imbalances, and possible social problems.

Figures of the week

Inflationary expectations in Russia are falling. In February, the expected level of inflation one year from now dropped to 11.9% (compared to 12.7% in January). Moreover, this time there is greater optimism among all respondents, according to the Central Bank’s latest survey. Long-term inflationary expectations are also down: the anticipated rate in five year’s time fell to 9.3%. Russia’s index of consumer confidence continues to rise.

Weekly inflation in Russia slowed in the week beginning February 13, dropping to 0.11% from 0.21% according to the Economic Development Ministry. The annual inflation rate remained unchanged at 7.57%.

Austria's Raiffeisen Bank said in its annual report this week that it has €477 million of funds stuck in Russian C-type accounts. It explained that these are payments received from Russian companies using “local debt instruments” that cannot be transferred to foreign investors due to sanctions. Raiffeisen also revealed it has paid $47 million windfall tax in Russia.

Further reading

Wars and elections: How European leaders can maintain public support for Ukraine

Russia’s Gas Export Strategy: Adapting to the New Reality

Navalny’s Death Highlights a New Global Division on Political Violence

Where do Russia’s mobilized soldiers come from? Evidence from bank deposits

{kind=link}