Russia’s economy after four years of war

Hello! Welcome to your weekly guide to the Russian economy, written by Alexandra Prokopenko and Alexander Kolyandr and brought to you by The Bell. Ahead of the anniversary of Russia’s invasion on February 24, we analyze the irreversible changes the Russian economy has gone through in the four years of the war.

Russia’s economy is unrecognizable from before the invasion. It might never go back

When Russia invaded, Western countries imposed sanctions that had previously been unimaginable. Many people, both inside Russia and abroad, expected a rapid economic collapse. That did not happen. The economy did not collapse. But it changed in a way that appears to be completely irreversible.

As the war enters its fifth year, the authorities continue to maintain an illusion of normalcy. Packed restaurants serve sanctioned wine, Russians fly on vacation to Turkey and Thailand, couriers deliver consumer goods to apartment blocks around the clock. At first glance, life goes on.

But such normalcy is becoming increasingly expensive. And we’re not talking only about record military spending or rising prices. Over the past four years, the very fabric of economic life in Russia has changed — how people and businesses pay for stuff, how the internet functions, who owns property, even how safe it is to live in your own home. Repression and censorship are also intensifying, working in tandem with high government spending to prop up this “illusion of normality.”

This week we highlight seven ways in which Russia’s economy of 2026 is markedly, perhaps forever, different from that of 2021.

Drone attacks

“It’s very hard to confuse the sound of a drone with anything else. It’s like someone is riding a moped across the sky carrying a bomb. It’s pretty scary when a bomb is flying over your head,” a former high-ranking Russian official told The Bell.

Ukrainian drones regularly fly over his home in the Odintsovo district near Moscow — attempted retaliatory attacks for the thousands Russia fires at Ukraine every month. Hits are much rarer in Russia than they are in Ukraine, though the damage has still been racking up. Ukraine even in 2023 managed to hit the top of the Kremlin in one attack, branded by Vladimir Putin’s spokesman as an assassination attempt.

Before 2022, there had not been a single drone attack on Russian territory in history. In 2025 alone, 8,300 so-called military incidents were recorded in Russia and the annexed Crimean peninsula. Nearly half were alleged Ukrainian drone attacks. According to Novaya Gazeta Europe, around 11 drone strikes or crashes and nine successful interceptions were recorded each day last year.

Ukrainian drones have even flown as far as Siberia, hitting an oil refinery in Russia’s Tyumen region on October 6. And in one of the most audacious strikes of the entire war by either side, Ukraine smuggled drones into Russia, launching them at bases housing Russia’s strategic bomber fleet in June 2025.

Bloomberg estimates Ukraine carried out 120 attacks on oil facilities in 2025. Most were refineries (81), the rest production sites (27), pipelines (8) and tankers (4). The direct and, in particular, the indirect losses to Russia from the strikes are difficult to calculate. Insurance companies report that loss ratios for “terrorism” and “sabotage” events have at least doubled compared to 2024. One insurance brokerage estimated direct losses in the oil and gas sector from drone strikes at 100 billion rubles ($1 billion), and more than 1 trillion rubles ($10 billion) in lost profits and indirect damage.

So far, the attacks on industrial facilities have not led to a major crisis, despite widespread reports of fuel shortages at gas stations last summer. Nevertheless, they have created a permanent threat and ongoing additional costs for repair and protection. The state has largely shifted the responsibility for footing this bill onto the companies.

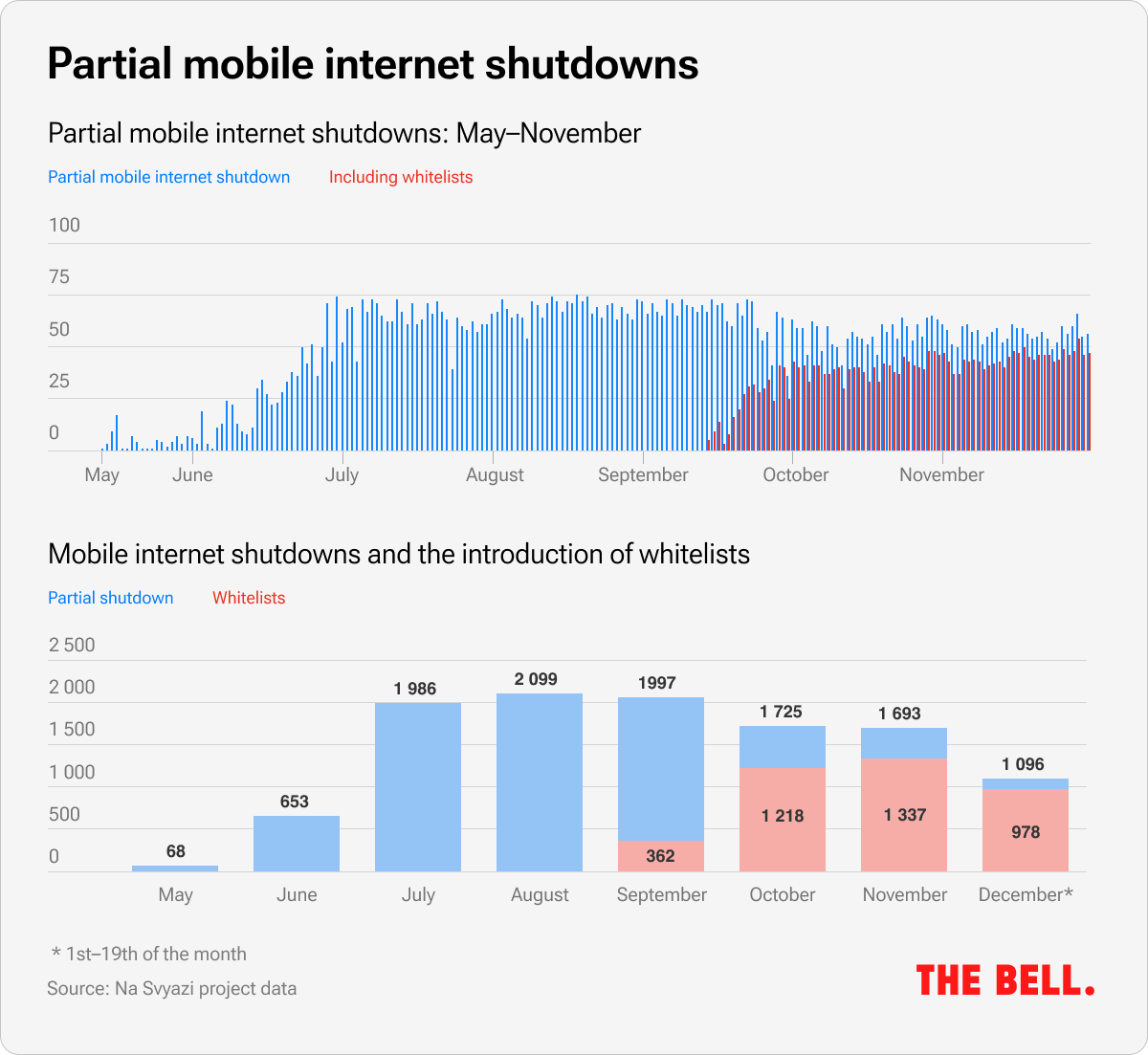

Communications shutdowns

In 2021, Russia ranked sixth in the world in terms of internet accessibility. Some 85% of the population — 124 million people — were online and mobile internet worked across the entire country, from Kaliningrad to Vladivostok.

By 2025, residents of dozens of Russian regions faced regular mobile internet blackouts as the authorities shut down connectivity in an attempt to counter drone threats, mostly without prior warning.

The internet blackouts mean people cannot properly use taxis, car sharing, scooter rentals, or order food and grocery deliveries. Many payment terminals and ATMs also stop working. In August 2025 alone, there were 2,129 shutdowns across Russia — more than were registered in the entire world in 2024. A country that once ranked among the top ten in digitalization became the global leader in internet shutdowns.

When the switch-offs became widespread, and acknowledged by the Kremlin, the authorities began compiling “white lists” — a limited set of online services that should remain accessible even during outages. Ultimately, Yandex services, marketplaces, VK social networks, and of course the national messenger Max, alongside banking apps, made it onto the approved lists. Putin’s friend Yuri Kovalchuk is among the shareholders of most of the apps included. Meanwhile users complain that even apps on the white list are not guaranteed to work well during the forced outages.

“Now we communicate more in person with friends and acquaintances. We read books, visit each other, drink tea,” residents of the million-strong city of Voronezh joke ironically. During his end-of-year call-in show, Vladimir Putin warned that people should not expect internet shutdowns to end any time soon. He was answering a question from somebody urging that glucose monitoring services for insulin-dependent children be added to the white list.

The state’s future intentions regarding the internet are best illustrated by a law passed by the State Duma this week that significantly simplifies the ability for the security services to implement a full internet shutdown. The original draft envisioned a separate list of cases in which this would be allowed. By the second reading, that provision had disappeared. Apparently, Russian authorities have taken note of Iran’s recent experience of ordering a complete nationwide shutdown during the recent protests. We wrote about this in more detail here.

2025 was also the year Russia finally became bold enough to completely shut down the previously throttled YouTube and block the most popular messengers — WhatsApp, and now Telegram. The blocking of the latter even led to communication disruptions on the front line among Russian military personnel, who actively use the messenger for coordination. Authorities in border regions have complained, since they use Telegram channels to inform local residents about air raid alerts.

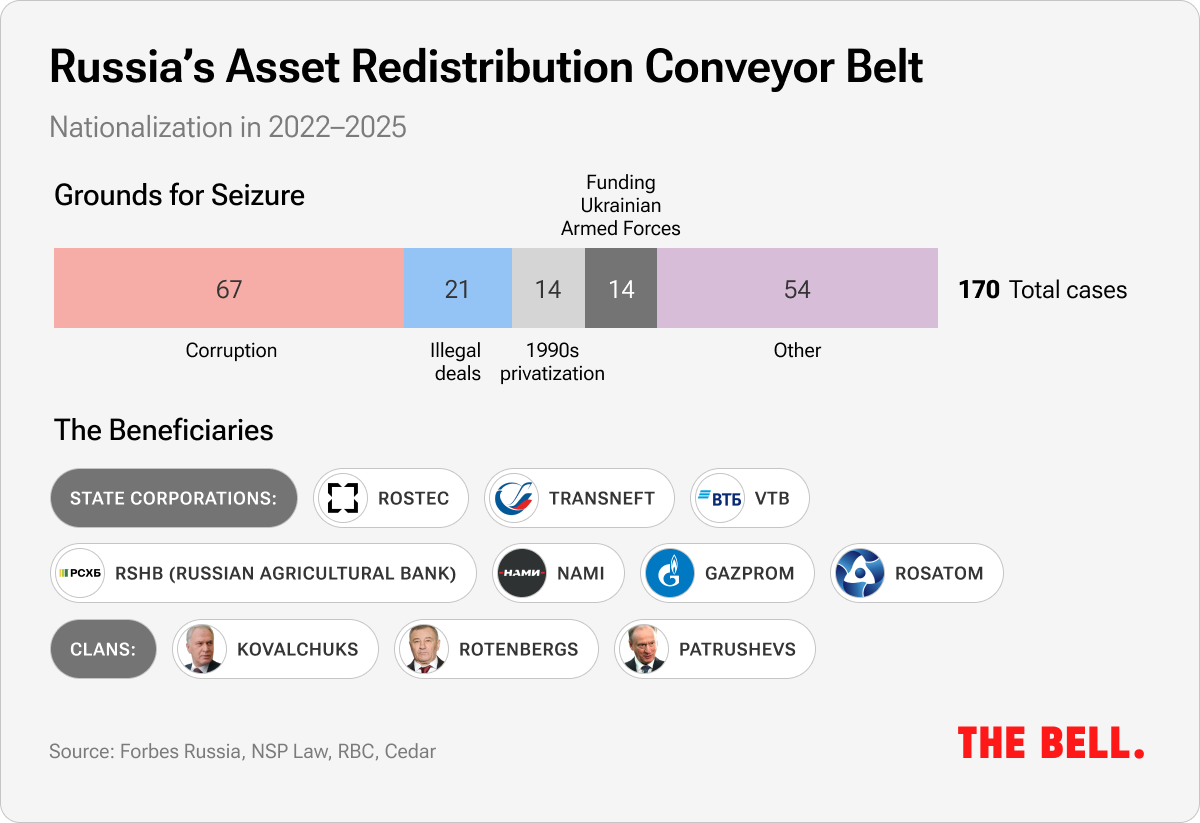

Nationalization

Before 2022, cases of nationalization in Russia were relatively rare. The state seized assets only in exceptional cases, usually linked to high-profile criminal prosecutions. After the invasion, that approach changed radically. The confiscation of private property became a routine instrument of economic policy.

The scale of the process is clearly visible in the numbers. In 2025, courts ordered the transfer of assets worth a total of $11.03 billion into state ownership — three times more than the year before ($3.89 billion). The share of nationalization in the total volume of mergers and acquisitions rose from 7.2% to 27.6%. In other words, more than a quarter of the entire Russian M&A market in 2025 was forced transfers to the state.

The largest nationalization was worth $4.3 billion after the Prosecutor General’s Office concluded Far Eastern businessman Oleg Kan had illegally acquired his “crab empire”. In second place was the nationalization of 67.85% of shares in the gold-mining company Yuzhuralzoloto (worth about $2 billion). The takeover of Moscow’s Domodedovo Airport was the most high-profile and particularly symbolic. Owner Dmitry Kamenshchik had been successfully resisting the state’s attempts to take over his business since the mid-2000s, but his luck ran out.

In total, since 2022, according to various estimates, the state has seized assets worth between 4.3- 6.5 trillion rubles ($56-84 billion) — four times the value of the companies sold during the infamous loans-for-shares auctions of 1995. Over the past three years, 411 companies have been nationalized.

The mechanism for nationalization is well established and simple. The Prosecutor General’s Office files a lawsuit alleging violations during the 1990s privatization of a certain company, suspicion of corruption, or threats to national security. At the end of 2024, the statute of limitations for such cases was effectively abolished, putting even 30-year-old transactions at risk of being reviewed. An additional risk is if the owners are foreign or have foreign citizenship alongside their Russian passports. Domodedovo’s Kamenshchik, for example, was accused of “following the aggressive policies of Western states” because he held residence permits in the UAE and Turkey (not exactly Western states). The economic consequences are obvious: when any asset can be seized by court order, long-term investment loses all sense.

The prosecutor’s office almost always wins — even if a court initially rules otherwise. In 2025, three out of four major court cases that had previously been decided in favor of owners were overturned.

High-profile cases are only the tip of the iceberg. Alongside the seizure of billion-dollar assets, regional courts are considering dozens of lawsuits over far more modest properties: sanatoriums, former pioneer camps, shopping centers, and land plots. In Primorye, prosecutors are seeking the return of 39 former children’s camps. In Krasnodar Krai, the Kanevsky District Court seized 372 properties belonging to the Pokrovsky agricultural conglomerate. In Sochi, the Lazarevsky Court is dealing with a case over 12 hectares of land of a former sanatorium.

In the occupied territories of Ukraine, a mechanism of mass housing confiscation from ordinary citizens is being tested. From August 2022 to October 2025, more than 4,000 properties (apartments and houses whose owners fled the war or refused to obtain Russian passports) were entered into registers of “ownerless property”. A commission inspects homes, and if no one is present, the property is added to the registry and transferred to the state after one year. In December 2025, the State Duma legalized this practice at the federal level. Confiscated housing is handed over to military personnel, occupation administration officials, and “resettled Russians.”

Officially, the Russian constitution protects private property rights. However, a bill allowing property seizure for “discrediting the army” has already been approved by the State Duma.

Nationalization has ceased to be a tool for exerting rare and highly targeted pressure on specific large businesses. It is now more of an assembly line operating at all levels of the judicial system, negatively affecting investment appetite and business sentiment. The effect will not be immediate — it will emerge in 5–10 years, once a critical mass of cases and seized assets accumulates.

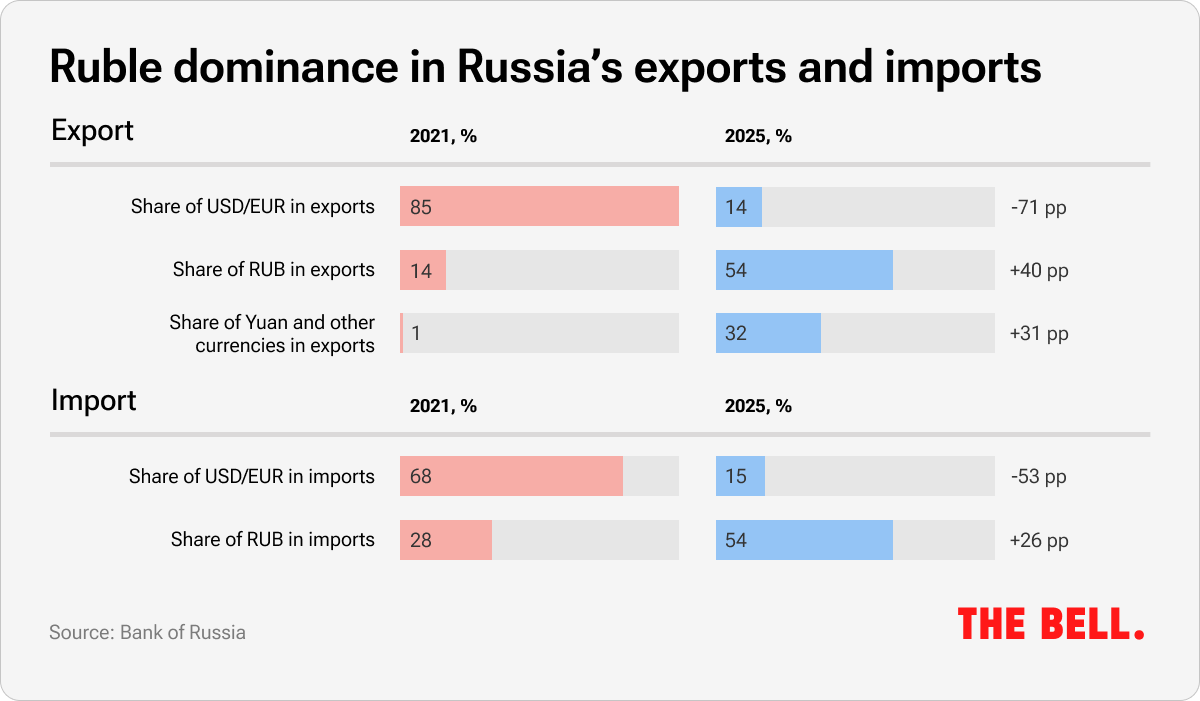

Foreign payments

Central Bank statistics show a tectonic shift in the currency structure of Russian foreign trade. At the beginning of 2022, the dollar and the euro were used in payments for 87% of Russian exports, while the ruble accounted for 12.4% and the yuan for 0.4%. By 2025, the situation had reversed completely: the ruble now accounts for 54% and the yuan for 32%. A similar trend has played out in imports.

At first glance, this looks like successful “de-dollarization.” In practice, Russia had no choice. After sanctions were imposed on the Central Bank and major banks were banned from operating in dollars and euros, Russia was forced to build an alternative payment infrastructure. Every transaction that takes place in the new system is more expensive, slower, and riskier than in the old one. The yuan is not freely convertible, and ruble settlements are limited to a small number of countries willing to accumulate Russian currency.

It is not just the currency choice that has been affected, but also the methods of payment. Until June 2024, Russian businesses paid Chinese suppliers directly, with a commission of about 1.5%, and the money arriving within a few days. But then the Moscow Exchange and the National Clearing Center were sanctioned and in December 2024, the United States threatened secondary sanctions against banks conducting operations with Russia. Banks in China, Turkey, and the UAE largely stopped accepting payments from Russia and businesses were forced to look for workarounds.

Payment agents became a popular solution — middlemen that conceal the Russian origin of funds. In general terms, the scheme works as follows: a Russian importer transfers money to a Russian agent, who sends it to a foreign sub-agent, the funds then pass through a chain of companies in Hong Kong, the UAE, Turkey, or Kazakhstan, and only then reach the Chinese supplier. The more links in the chain, the harder it is to trace the connection to Russia. But the price of such “invisibility” ranges from 3% to 8% of the total transaction. Taking into account currency losses, delays, and freezing risks, the total costs can reach 15–20% of any deal.

The market for payment agents has exploded. Before sanctions, 15–20% of payments to China went through intermediaries. By the end of 2024, it was 70–80%. But such a fresh market brings risks, primarily related to fraud. Agents can appear and disappear, leaving money stuck in intermediary accounts. Businesses are often forced to work with counterparties about whom nothing is known except a Telegram number.

And that is just the mechanism for regular goods. Much more complex schemes have popped up to service the import of sanctioned goods and dual-use products like electronics and machine tools into Russia. Payments there are virtually impossible without more steps since Chinese banks refuse them even with intermediaries involved. The goods must be reclassified, shipments split up, and physically routed through third countries. Each stage adds time and cost.

Sanctions have not stopped Russia trading with the world, but they have made it more expensive, slower, and riskier. Ultimately, these costs are paid by the consumer.

Logistics headaches

Four years of war have transformed Russia’s logistical links with the rest of the world beyond recognition. Direct air connections with the West were ended almost immediately as the EU, US and Canada closed their airspace to Russian aircraft. Russia responded by doing the same for Western planes. The vast links of connectivity with the West, built up over three decades following the collapse of the Soviet Union, disappeared in a matter of hours.

Before the Covid pandemic, Russia had direct air connections with 69 countries and was an integral part of the global aviation network. Major Russian airlines belonged to international alliances, and flights between the West and Asia crossed over Russian territory — the shortest flight path. Overflights through the Trans-Siberian air corridor earned Russia approximately $500–800 million a year in fees from Western airlines.

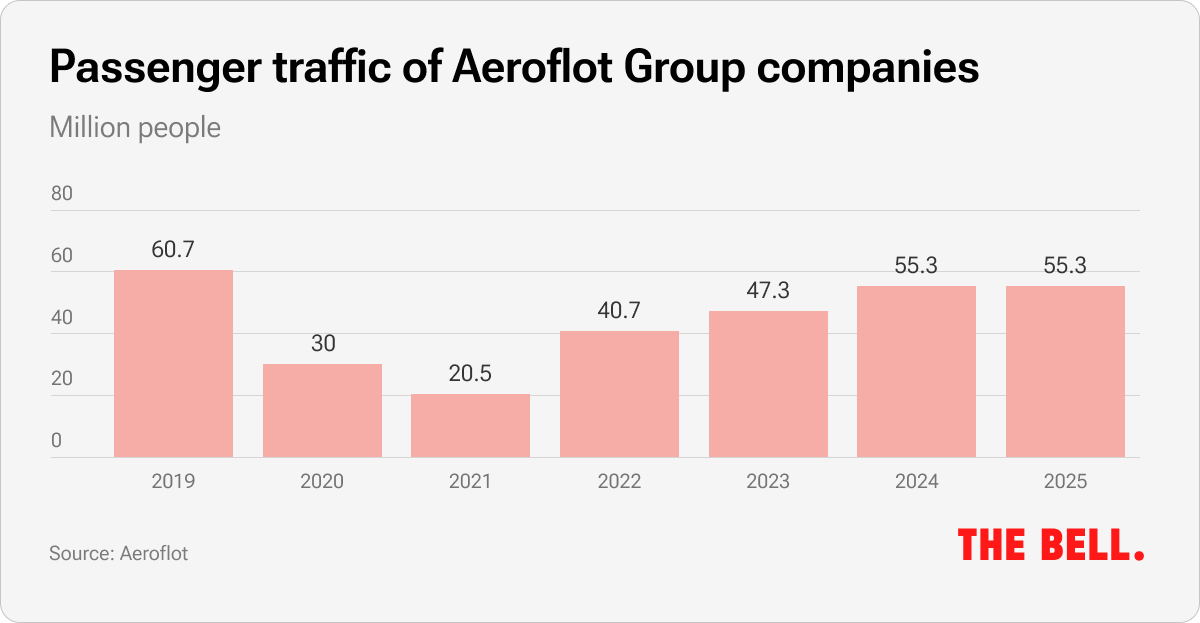

Today, the number of countries with direct air connections to Russia has fallen to 42. There are no direct flights to Europe (except Serbia), with all the main routes heading to Asia. Nearly half of all Russia’s outbound flights go to hub airports in Turkey and the Gulf. Flag carrier Aeroflot has never managed to hit pre-pandemic passenger volumes. For anybody travelling to Europe, fares have become several times more expensive, longer, and more complicated. For Russia’s domestic aviation industry, sanctions have made it increasingly costly and difficult for airlines to purchase spare parts and carry out maintenance.

The fate of air travel is the most obvious demonstration of Russia’s completely transformed logistics landscape following its invasion. But the impact is much deeper. Direct shipments to Russia from European manufacturers have become rare. Allowing parallel imports solved the legal problem, but logistical and financial costs have ballooned, all of which were passed on to shoppers. Outside the consumer market, the problem has been even more serious, especially with regard to machine tools, spare parts, and consumables. Dependence on China has increased, and where Western imports are required — especially for sanctioned goods — prices rose sharply.

In some respects, this stimulated domestic production, but manufacturers also became hostages of policy. If a deal is reached with Ukraine that involves the lifting of Western sanctions, they may prove uncompetitive and lose their market share. It’s unclear how Russia’s much-touted pivot to the East would hold up if the ability to choose suppliers based on price, logistics, and quality becomes easier and simpler once again. In any case, a return to Russia’s pre-war status quo in terms of logistics and its geographical trading patterns, would be difficult and unlikely to be quick.

Western firms gone

Western companies had been steadily entering the Russian market since the 1990s. Growing purchasing power, greater legal protection, intellectual property rights, and the deregulation of taxes and fees meant that, on the surface, Russia looked little different from consumer markets in the likes of Spain, France or Turkey. There were similar brands, similar products and roughly the same prices. That had already begun to change in 2014 following the annexation of Crimea. While Western firms stayed, the Kremlin closed its markets to European food and agricultural imports, under the pretext of responding to Western sanctions.

With the invasion, many Western companies left Russia, either for moral reasons or because the business risks were too high. Moscow quickly moved to permit parallel imports – the ability to buy foreign goods without having the permission of the trademark holder. In other words, Russian retailers could carry on buying iPhones through middlemen even though Apple wasn’t officially selling them to Russia. The aim was to prevent shortages and avoid a sudden disappearance of goods that Russians had come to know and rely on. It was also needed to keep the flow of industrial parts, materials and machine tools coming into the country. For the most part, within a year, imports were proceeding as they had in the 1990s, using various workaround schemes. This hit quality, availability and prices.

In many ways, Russia’s consumer market has not changed too much. Imported cars from Europe have been replaced with vehicles from China. Western brands have been replaced by Russian alternatives with new clunky names — but the products remain much the same. iPhones are available and selling at European prices. In short, Russian copies, Chinese equivalents, outright counterfeits or expensive parallel imports have filled the market.

The example of Coca-Cola, market leader for sodas with 26% of the market, is illustrative. Until 2022, the company operated 10 factories in Russia. After the invasion, it ceased imports and manufacturing in Russia. Soon Russia became flooded with imitations under different brand names. Notably they included “Dobry Cola”, which was produced at the same factories by Swiss company, Coca-Cola HBC, 21.3% of which is owned by the US Coca-Cola). Original Coca-Cola is still available — imported from the likes of Iran, Uzbekistan, Poland, Britain and even Afghanistan. It goes for twice the price of the local versions, and cost slightly more than in Britain. Imported soda now accounts for 6.5% of the market, with a strong ruble and pre-war tastes helping well-heeled Russians hang on to their pre-war drinking habits.

Sweden’s IKEA is another example. It entered Russia in 2000, at the very start of Putin’s presidency. It became a symbol of Russia’s revitalized economy following the 1998 crisis, a testament to normalization and integration into European and global markets. By the start of the war, IKEA had 17 stores and other factories and assembly sites. It left in 2022. Yet furniture, identical in size and design, is still being made in Russian factories that openly acknowledge they are catering to the desire for a “familiar style.” IKEA’s newer models are not available, and the old ones retail for at least 50% more than in Europe.

Russian law no longer protects the rights of trademark holders from unfriendly countries. Russian pharmacists actively produce generic versions of Western drugs, regardless of patents. Last year, for example, the Supreme Court dismissed a patent dispute between Danish pharmaceutical company Novo Nordisk and the Russian government. Novo Nordisk sought to prevent Russian companies from using its patent to produce obesity drugs based on Ozempic. But its lawsuit failed, even though the company remained active in Russia after 2022.

Russia’s authorities are no longer bothering to try to stop the spread of pirated software, while pirated films have proliferated since Western moviemakers halted big screen releases in Russia. Leading cinema chains have even started showing bootleg copies of Hollywood movies. Technically, viewers buy a ticket for a little-known short Russian film, after which the Hollywood blockbuster is shown as a bonus freebie. But due to high ticket prices and the widespread availability of such films online, fewer and fewer people are going to the movies.

There are many other examples about the spread of copycat and workaround products — and not just in the consumer sector. Manufacturing companies complain about counterfeit Chinese ball bearings being passed off as more expensive and rare Russian ones amid a near complete absence of Western ones. Those who own European cars lament counterfeit or unaffordable spare parts, while dentists too bemoan inferior materials.

In short, Russia’s post-Soviet model of legal foreign trade, the gradual localization of production and narrowing price gaps with Europe — one that took three decades to build — collapsed in the space of three years.

In its place, the import practices of the 1990s are back — high prices, disregard for patents and trademarks, goods of unclear origins and widespread piracy. It is often dubbed the “Abibas” model, a reference to the misspelled brand name on cut-price bootleg sneakers sold at street markets after the collapse of the USSR.

An immediate turnaround will not be possible. Local and Chinese manufacturers won’t give up their new market share without a fight. Western companies that have been forced out of the country, had their assets essentially taken from them, trademark rights ignored, and their goods imported through the back door are hardly likely to be rushing back.

A two-sector economic model

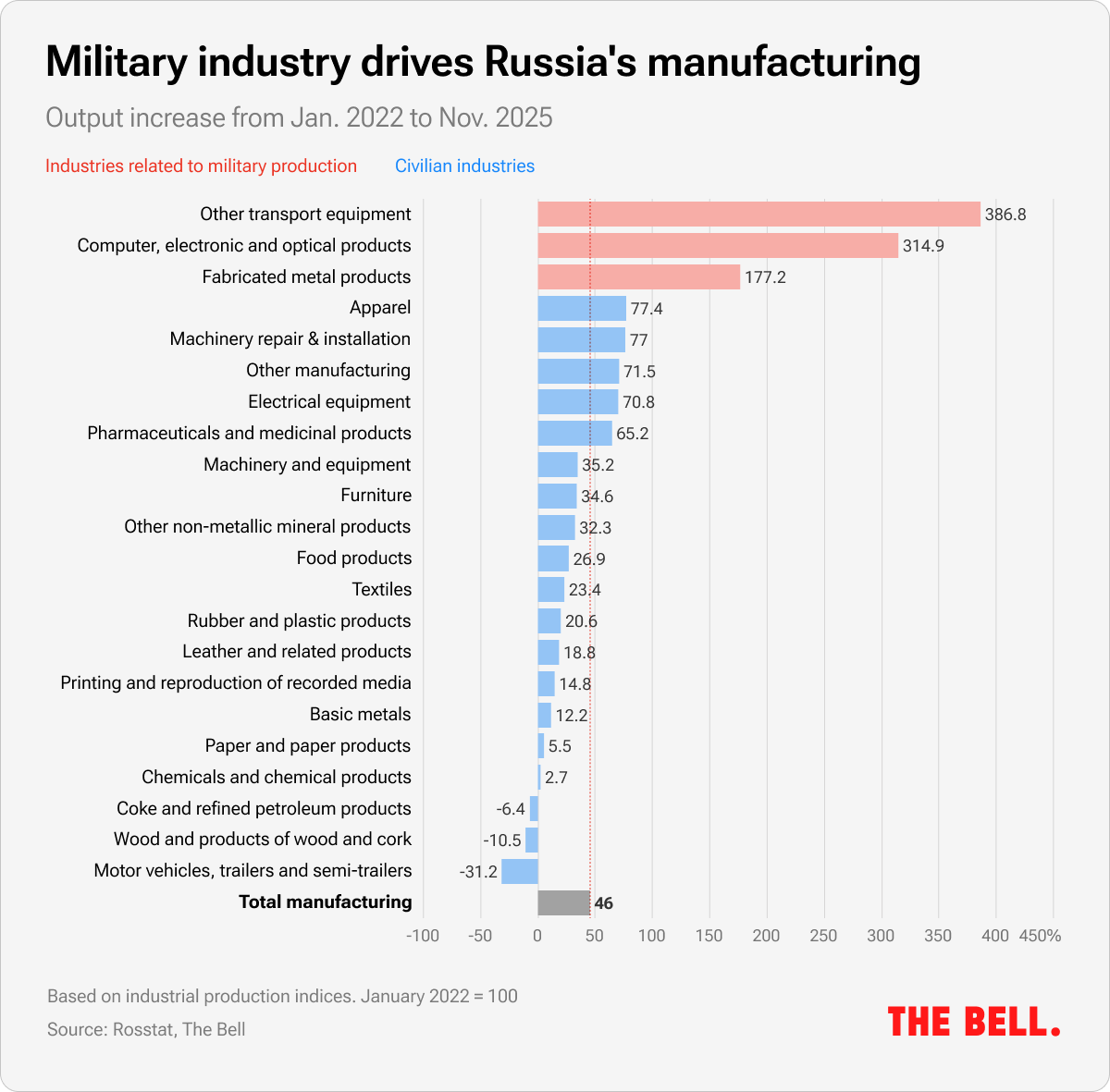

Four years of war has split the Russian economy in two. The military-related sector is flourishing with priority access to scarce resources: staff, capital, components and foreign currency. But private business and consumer sectors unrelated to the war are in decline amid sanctions pressure, taxes and prohibitively expensive borrowing.

The divergence is akin to an economic vacuum cleaner. High interest rates (15.5% now, but 21% in mid-2025) deprive civilian businesses of access to loans, while military parts of the economy get preferential credits. The labor shortage pushes up wages, but the military-industrial complex keeps paying more, hoovering up expertise. All of Russia’s logistics, energy resources and components go first to defense firms or the army directly, with the rest of the economy left to fight for the scraps.

In the first four years of the war, manufacturing as a whole went up 18.3%. But when broken down into military and civilian sectors, the picture changes. Defense industries accounted for all this growth and more: their contribution to the overall figure exceeded 20 percentage points. That means that civilian industries declined over the same period.

Today’s war rents serve the same function as the oil-and-gas windfalls of the early 2000s. They feed a privileged group and create the illusion of prosperity. But there is one critical difference. In the 2000s, the money was coming from exports, pouring into the country from abroad. Even after the elite took its slice, some was being redistributed through the budget, creating consumer and investment demand.

But now the state uses the same energy profits — albeit much reduced — to finance its war. Money is spent on tanks, drones and shells that are burning in Ukrainian fields. Extra cash goes to compensate the families of killed soldiers who have stopped earning a wage. There is zero multiplier effect. Resources simply disappear, the military behaves like a malignant cancer. The tumor grows and the overall bodyweight increases. On the scales, it looks like “growth”. But there is nothing of any valuable weight being added. It merely sucks blood, nutrients and oxygen from healthy tissue. The faster it grows, the weaker the body becomes.

Why the world should care

Four years of war have changed Russia more than the Kremlin is willing to admit. Drones over Moscow, internet shutdowns, the confiscation of property, webs of financial intermediaries, supply chain disruption, parallel imports, and an economy split into military and civilian sectors have all become the new normal. Some of these changes seem irreversible. Payment infrastructure, built over decades of integration with the world economy, has been wrecked. Its recovery, even without sanctions, is far from guaranteed. The experts and foreign firms who left the country will not return at the drop of a hat, if ever. Investor confidence, undermined by a wave of nationalizations, cannot be restored by a change of rhetoric. Civilian industries, starved of resources in favor of the military-industrial complex, cannot survive on their own.

Internal imbalances and external disruptions will continue to harm the economy long after the guns fall silent. The two-sector model, with a thriving military sector and civilian industry in the doldrums, has created structural imbalances that cannot be corrected simply by cutting military spending. Abrupt demilitarization will crash the economy, while maintaining the status quo will embed stagnation.

Even if Russia’s war on Ukraine ends in 2026, it will be a long journey back to normality. And if it even exists, the path will cost more than many anticipate.

French version edited by Marika Ruggiero, German version edited by Jan Möller

{kind=link}