Top construction firm asks state for help

Russia’s construction sector has become the first victim of ongoing high interest rates. Samolet, the country’s biggest construction firm, has appealed to the government for cheap credit to help it out of its tough financial situation.

- Samolet, the largest developer in terms of square footage under development (4.5 million square metres), asked the government for a subsidized three-year loan of 50 billion rubles ($650 million). The company is prepared to secure the loan with a stake in the company. Samolet believes its problems are short-term and surmountable, blaming them on high borrowing costs, the end of the preferential mortgage scheme and the scrapping of the moratorium of lawsuits against developers for missed deadlines.

- A market source told Forbes that the company has had problems for more than a year, and that it should not be seen as evidence of a wider crisis in the Russian construction sector. However, broader problems have been building up for some time and The Bell a year ago named the construction sector as one of the country’s top five problem industries.

- Samolet is asking for a lot. 50 billion rubles represents half of the anticipated annual income the state will get from legalizing online casinos. But the authorities cannot completely abandon a socially significant business. An equity stake or sale of an asset to a government-linked structure is more likely than a loan.

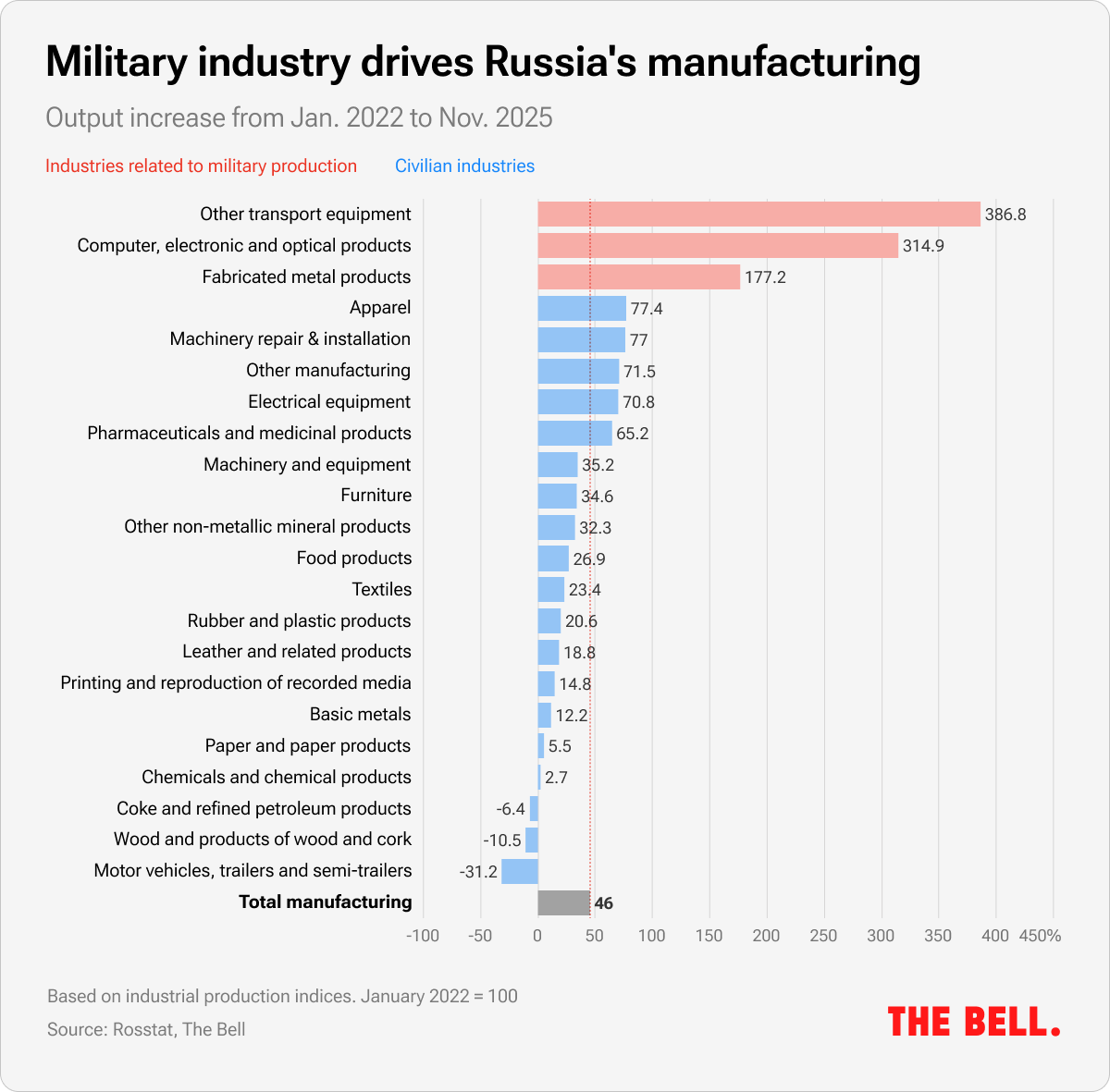

- Builders are far from the only industry on rocky foundations, being forced to look for state support — a mounting problem amid high interest rates and the contraction of the civilian part of Russia’s economy.

- This week the Russian Steel Association, which brings together the country’s biggest metals companies, was preparing to present a package of anti-crisis measures to the government. The industry is facing a fall in domestic demand which started back in 2024 when construction began to decline, imports increased, the strong ruble reduced the value of exports and sanctions hit traditional sales markets. The steelmakers are not asking for direct funding, but instead suggest legislation to stimulate demand, restrict imports and ease the requirements for the costly transfer to using Russian-produced software. It is not a direct call for state money like with Samolet, but granting the request would reduce budget revenues.

- Russian coal companies have faced big difficulties since last year as prices fall but transportation and tax bills go up. They are getting tax deferrals, targeted subsidies and discounts on rail freight services.

- Meanwhile, state rail monopoly Russian Railways has its own problems: a serious debt crisis requiring state support. The government has been discussing a rescue plan since December, which could cost up to 1.3 trillion rubles ($16.9 billion). With double-digit interest rates and reduced profits amid stalled economic growth, Russian Railways can no longer service its debts, which have almost tripled during the war from 1.5 trillion to 4 trillion rubles ($52 billion). The company is selling its skyscrapers and one of its service companies to manage debts without overburdening the budget. But even if, unlikely as it seems, Russian Railways manages to get by without a major government cash injection, its unprofitability means that this year it cannot make any dividend payments to the state.

- Russia’s largest oil company, Rosneft, also faces a fall in net profits, largely due to the inflated cost of servicing loans. Rosneft transfers a quarter of its profits to the treasury.

Why the world should care

The list of troubled companies and industries is getting longer as demand contracts amid increased costs to service loans and high inflation. In one sense, this is a consequence of the pumping of budget money into the economy from 2022 to 2024, causing rapid growth and overheating.

This perfect storm that will engulf entire industries has a lot in common with the global financial crisis of 2008-9. Unlike then, the state has no extra money for support, no opportunity to reduce military or social spending (its biggest outgoings) and sanctions mean there is no hope of a quick export-led recovery.

The problems we predicted a year ago are just starting to materialize. And the state is steadily losing options to throw money at them. As budget reserves are depleted, access to loans and state resources will depend less on efficiency and more on political and financial clout. The economy can still function without collapse, but room for maneuver is closing fast.

French version edited by Marika Ruggiero, German version edited by Jan Möller

{kind=link}